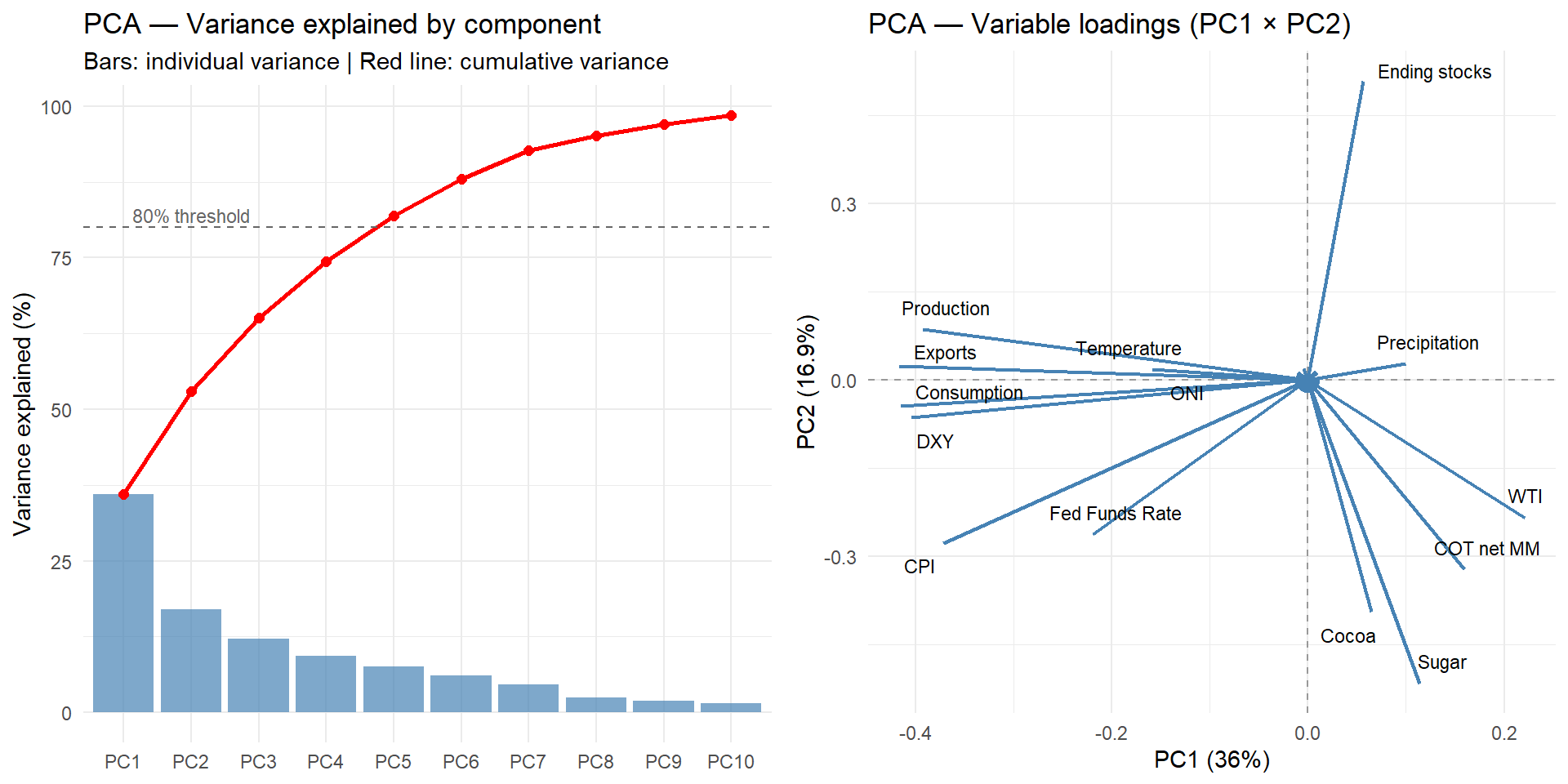

---

title: "Predicting Arabica and Robusta Coffee Futures Prices: A Machine Learning Approach with Macroeconomic, Climatic, and Speculative Determinants"

subtitle: "Master's Thesis in Management — Business Analytics Orientation"

author: "Mohamed Hussein"

date: today

institution: "HEC Lausanne, University of Lausanne (UNIL)"

supervisor: "M. Vialfont"

format:

html:

toc: true

toc-depth: 3

number-sections: true

theme: cosmo

code-fold: true

code-summary: "Show code"

code-tools: true

css: styles.css

lang: en

---

# Data

## Setup

This chunk initialises the working environment for the entire pipeline. All file paths and global constants are defined here and referenced in every subsequent chunk, so that no hard-coded paths appear elsewhere in the document. Constructing all paths relative to `BASE_PATH` ensures full reproducibility across machines: relocating the data folder requires editing a single line.

```{r setup, message=FALSE, warning=FALSE}

packages_requis <- c(

"readxl", "dplyr", "tidyr", "lubridate", "zoo", "readr",

"ggplot2", "corrplot", "tseries", "urca", "forecast",

"scales", "gridExtra", "knitr", "kableExtra", "moments",

"ggrepel", "randomForest", "xgboost", "e1071", "nnet",

"Metrics", "tibble"

)

for (pkg in packages_requis) {

if (!requireNamespace(pkg, quietly = TRUE)) {

install.packages(pkg, dependencies = TRUE)

}

}

invisible(lapply(packages_requis, library, character.only = TRUE))

# ----------------------------------------------------------

# ROOT AND SUBDIRECTORY PATHS

# BASE_PATH points to the data folder at the project root.

# All subdirectories are derived from it using file.path(),

# so moving the data folder only requires editing one line.

# ----------------------------------------------------------

BASE_PATH <- "Datasets mémoire de master"

PATH_CLIMATIQUES <- file.path(BASE_PATH, "Climatiques")

PATH_PRECIP <- file.path(BASE_PATH, "Climatiques", "Précipitations")

PATH_TEMP <- file.path(BASE_PATH, "Climatiques", "Températures")

PATH_REFINITIV <- file.path(BASE_PATH, "Extraction Refinitiv")

PATH_MACRO <- file.path(BASE_PATH, "Macroéconomique et financier")

PATH_COT <- file.path(BASE_PATH, "Spéculation ICE Arabica Hebdomadaire")

PATH_OUTPUT <- "output"

# Create output folders if they do not already exist

if (!dir.exists(PATH_OUTPUT)) dir.create(PATH_OUTPUT)

dir.create(file.path(PATH_OUTPUT, "tables"), showWarnings = FALSE)

# ----------------------------------------------------------

# INDIVIDUAL FILE PATHS — PRICE AND MACROECONOMIC DATA

# Daily futures prices are sourced from Refinitiv via CEDIF.

# Macroeconomic series are sourced from FRED, Investing.com,

# the USDA FAS PSD Online database, and the OECD.

# ----------------------------------------------------------

# Futures prices (daily, aggregated to monthly in later chunks)

FICHIER_ARABICA <- file.path(PATH_REFINITIV, "Arabica_Coffee_Daily_Price_Refinitiv.xlsx")

FICHIER_ROBUSTA <- file.path(PATH_REFINITIV, "Robusta_Coffee_Daily_Price_Refinitiv.xlsx")

FICHIER_CACAO_NY <- file.path(PATH_REFINITIV, "ICE_NY_Cocoa_Daily_Price_Refinitiv.xlsx")

FICHIER_SUCRE_11 <- file.path(PATH_REFINITIV, "Sugar_No.11_Daily_Price_Refinitiv.xlsx")

# Macroeconomic and fundamental variables

FICHIER_USDA <- file.path(PATH_MACRO, "Coffee_Green_Production_Consumption_Export_Yearly.xlsx")

FICHIER_CPI <- file.path(PATH_MACRO, "Inflation_CPI_Monthly_1990.csv")

FICHIER_WTI <- file.path(PATH_MACRO, "Prix_du_Pétrole_WTI_Monthly_1990.csv")

FICHIER_FED <- file.path(PATH_MACRO, "Taux_Directeur_FED_Monthly_1990.csv")

FICHIER_DXY <- file.path(PATH_MACRO, "US_DXY_Index_Monthly_Historical_Data_1990.csv")

FICHIER_PIB <- file.path(PATH_MACRO, "Quarterly_GDP_OECD_from_2000_to_2025.xlsx")

# ENSO climate index

FICHIER_ONI <- file.path(PATH_CLIMATIQUES, "Index_ONI_Monthly_LONG_Format_1950.xlsx")

# ----------------------------------------------------------

# CLIMATE DATA FILE LISTS — 14 PRODUCER COUNTRIES

# ERA5 reanalysis data (World Bank CCKP, ADM1 resolution)

# is stored as one file per country per climate variable.

# The list names match the internal identifiers used when

# computing production-weighted climate indices downstream.

# Only countries with an average production share >= 1%

# over 2000-2024 are retained (see chunk `selection_pays`).

# ----------------------------------------------------------

FICHIERS_PRECIP <- list(

bresil = file.path(PATH_PRECIP, "précipitations_brésil_1950_2023_monthly.xlsx"),

vietnam = file.path(PATH_PRECIP, "précipitations_vietnam_1950_2023_monthly.xlsx"),

colombie = file.path(PATH_PRECIP, "précipitations_colombie_1950_2023_monthly.xlsx"),

indonesie = file.path(PATH_PRECIP, "précipitations_indonésie_1950_2023_monthly.xlsx"),

ethiopie = file.path(PATH_PRECIP, "précipitations_éthiopie_1950_2023_monthly.xlsx"),

inde = file.path(PATH_PRECIP, "précipitations_inde_1950_2023_monthly.xlsx"),

honduras = file.path(PATH_PRECIP, "précipitations_honduras_1950_2023_monthly.xlsx"),

mexique = file.path(PATH_PRECIP, "précipitations_mexique_1950_2023_monthly.xlsx"),

uganda = file.path(PATH_PRECIP, "précipitations_ouganda_1950_2023_monthly.xlsx"),

guatemala = file.path(PATH_PRECIP, "précipitations_guatemala_1950_2023_monthly.xlsx"),

perou = file.path(PATH_PRECIP, "précipitations_pérou_1950_2023_monthly.xlsx"),

cote_ivoire = file.path(PATH_PRECIP, "précipitations_côte_d_ivoire_1950_2023_monthly.xlsx"),

nicaragua = file.path(PATH_PRECIP, "précipitations_nicaragua_1950_2023_monthly.xlsx"),

costa_rica = file.path(PATH_PRECIP, "précipitations_costa_rica_1950_2023_monthly.xlsx")

)

FICHIERS_TEMP <- list(

bresil = file.path(PATH_TEMP, "températures_brésil_1950_2023_monthly.xlsx"),

vietnam = file.path(PATH_TEMP, "températures_vietnam_1950_2023_monthly.xlsx"),

colombie = file.path(PATH_TEMP, "températures_colombie_1950_2023_monthly.xlsx"),

indonesie = file.path(PATH_TEMP, "températures_indonésie_1950_2023_monthly.xlsx"),

ethiopie = file.path(PATH_TEMP, "températures_éthiopie_1950_2023_monthly.xlsx"),

inde = file.path(PATH_TEMP, "températures_inde_1950_2023_monthly.xlsx"),

honduras = file.path(PATH_TEMP, "températures_honduras_1950_2023_monthly.xlsx"),

mexique = file.path(PATH_TEMP, "températures_mexique_1950_2023_monthly.xlsx"),

uganda = file.path(PATH_TEMP, "températures_ouganda_1950_2023_monthly.xlsx"),

guatemala = file.path(PATH_TEMP, "températures_guatemala_1950_2023_monthly.xlsx"),

perou = file.path(PATH_TEMP, "températures_pérou_1950_2023_monthly.xlsx"),

cote_ivoire = file.path(PATH_TEMP, "températures_côte_d_ivoire_1950_2023_monthly.xlsx"),

nicaragua = file.path(PATH_TEMP, "températures_nicaragua_1950_2023_monthly.xlsx"),

costa_rica = file.path(PATH_TEMP, "températures_costa_rica_1950_2023_monthly.xlsx")

)

# ----------------------------------------------------------

# COT FILE LIST — CFTC DISAGGREGATED FUTURES-ONLY REPORTS

# The CFTC provides one consolidated file covering June 2006

# to 2015, followed by individual annual files from 2016

# onward. All files are read and stacked in chunk `cot`.

# ----------------------------------------------------------

FICHIERS_COT <- c(

file.path(PATH_COT, "juin_2006-2015.xls"),

file.path(PATH_COT, "2016.xls"), file.path(PATH_COT, "2017.xls"),

file.path(PATH_COT, "2018.xls"), file.path(PATH_COT, "2019.xls"),

file.path(PATH_COT, "2020.xls"), file.path(PATH_COT, "2021.xls"),

file.path(PATH_COT, "2022.xls"), file.path(PATH_COT, "2023.xls"),

file.path(PATH_COT, "2024.xls")

)

# ----------------------------------------------------------

# GLOBAL TIME CONSTANTS

# These bounds are applied as filters in every subsequent

# chunk, ensuring strict temporal consistency across the

# entire dataset assembly and modelling pipeline.

# ----------------------------------------------------------

DATE_DEBUT <- "2000-01" # Start of the main analysis period

DATE_FIN <- "2023-12" # End of the main analysis period

DATE_DEBUT_COT <- "2006-06" # First available COT observation (June 2006)

```

## Overview of the Dataset

This study draws on eight distinct data sources covering the period from January 2000 to December 2023, yielding 288 monthly observations for the main analysis and 96 quarterly observations for specifications that incorporate GDP growth. The analysis period begins in 2000 for three converging reasons. First, the suspension of the International Coffee Organization's export quota system in 1989 and its definitive abandonment in the early 1990s led to a decade of institutional transition, culminating in the 2001 ICO reform that established the fully liberalised price regime that prevails today. Data prior to 2000 therefore reflect a structurally different market environment and would introduce regime-change breaks that complicate time series modelling. Second, the ERA5 reanalysis dataset used for climate variables reaches its highest spatial and temporal reliability from the late 1990s onward, as the assimilation of satellite observations improves significantly over this period. Third, several key variables — including the CFTC Disaggregated COT report and Robusta futures prices from Refinitiv — are either unavailable or unreliable before this period. The analysis ends in December 2023, the last month for which all data sources are simultaneously available at the time of data collection.

This chunk produces the variable summary table presented in the text. Each row corresponds to one variable retained in the final dataset, grouped by category. The table is built manually as a data frame so that the ordering and grouping of rows can be controlled precisely, then rendered using `kableExtra` with row-merging on the Category column for readability.

```{r table_variables}

# Build the variable inventory as a structured data frame.

# Rows are ordered by category first, then by variable role

# within each category (dependent before regressors, etc.).

table_vars <- data.frame(

Category = c(

"Dependent", "Dependent",

"Spillovers", "Spillovers",

"Macroeconomic", "Macroeconomic", "Macroeconomic", "Macroeconomic",

"Macroeconomic",

"Fundamentals", "Fundamentals", "Fundamentals", "Fundamentals",

"Speculation",

"Climate", "Climate", "Climate"

),

Variable = c(

"Arabica futures price (ICE/NYBOT)",

"Robusta futures price (LIFFE)",

"Sugar No.11 futures price (ICE)",

"Cocoa futures price (ICE NY)",

"WTI crude oil price",

"US Dollar Index (DXY)",

"Federal Funds Rate",

"US Consumer Price Index (CPI)",

"OECD real GDP growth rate",

"World coffee production",

"World coffee consumption",

"World coffee exports",

"World ending stocks",

"Managed Money net position (COT)",

"Weighted precipitation index (14 countries)",

"Weighted temperature index (14 countries)",

"Oceanic Niño Index (ONI)"

),

Source = c(

"Refinitiv / CEDIF (UNIL)",

"Refinitiv / CEDIF (UNIL)",

"Refinitiv / CEDIF (UNIL)",

"Refinitiv / CEDIF (UNIL)",

"FRED (Federal Reserve)",

"Investing.com",

"FRED (Federal Reserve)",

"FRED (Federal Reserve)",

"OECD Data Explorer",

"USDA FAS PSD Online",

"USDA FAS PSD Online",

"USDA FAS PSD Online",

"USDA FAS PSD Online",

"CFTC Disaggregated Futures-Only",

"World Bank CCKP (ERA5 0.25°)",

"World Bank CCKP (ERA5 0.25°)",

"NOAA"

),

Frequency = c(

"Monthly", "Monthly (from 2008)",

"Monthly", "Monthly",

"Monthly", "Monthly", "Monthly", "Monthly",

"Quarterly",

"Annual (expanded to monthly)",

"Annual (expanded to monthly)",

"Annual (expanded to monthly)",

"Annual (expanded to monthly)",

"Monthly (from June 2006)",

"Monthly", "Monthly", "Monthly"

),

stringsAsFactors = FALSE

)

# Render the table with merged category cells and striped rows.

# collapse_rows() merges consecutive identical values in the

# Category column, avoiding visual repetition in the output.

kable(table_vars,

caption = "Summary of variables, sources and frequencies",

col.names = c("Category", "Variable", "Source", "Frequency"),

booktabs = TRUE) %>%

kable_styling(bootstrap_options = c("striped", "hover"),

font_size = 11, full_width = TRUE) %>%

collapse_rows(columns = 1, valign = "middle")

```

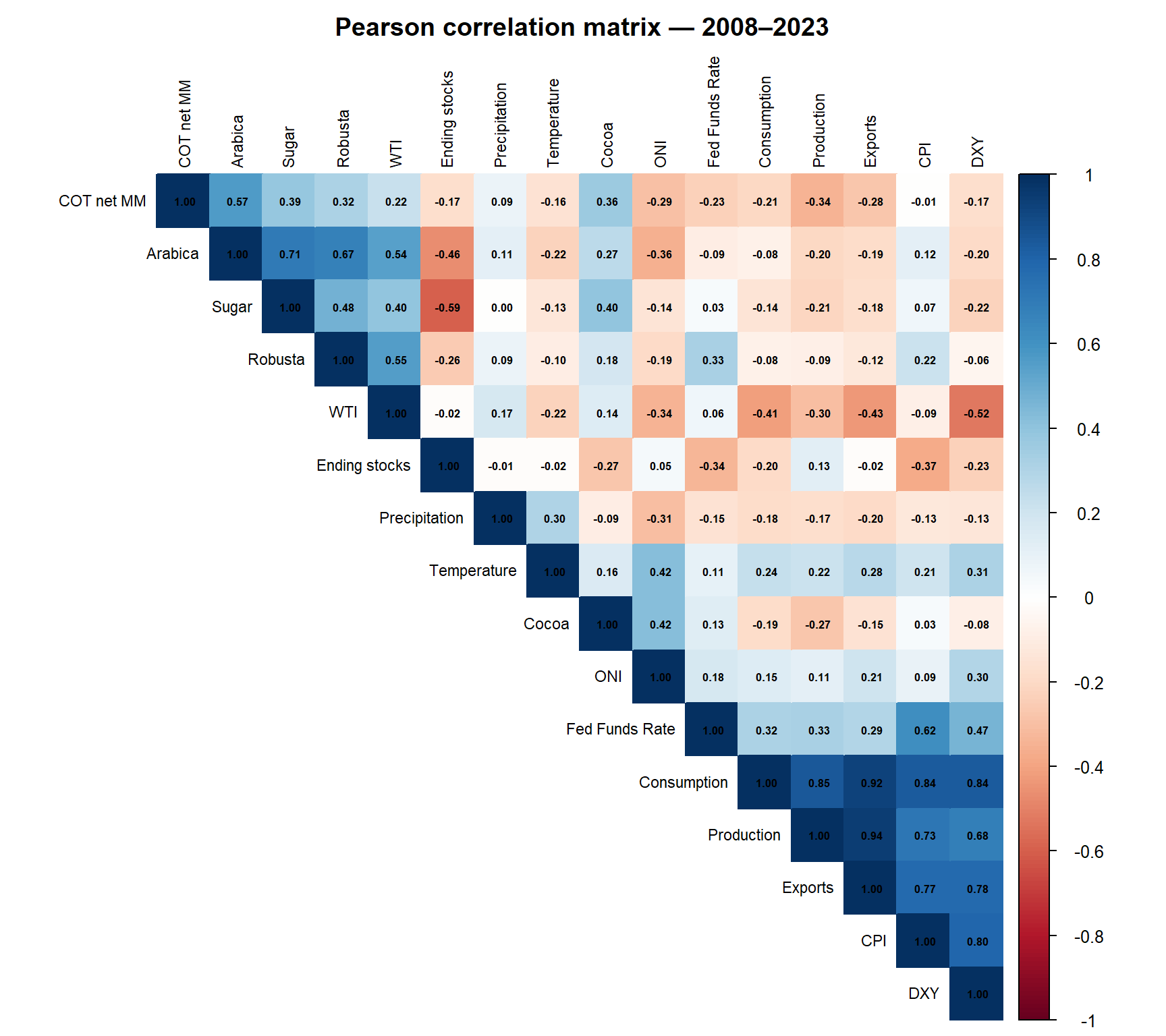

Two data availability constraints deserve explicit acknowledgement. First, Robusta futures prices from Refinitiv are available only from 2008 onward; the 96 months spanning 2000–2007 are therefore missing for this variable, and Robusta models are estimated on the 2008–2023 sub-period. Second, the CFTC Disaggregated COT report — which distinguishes Managed Money from commercial traders — was introduced in June 2006. The net speculative position variable accordingly contains missing values for the 2000–2006 period, which is documented and handled in the modelling phase.

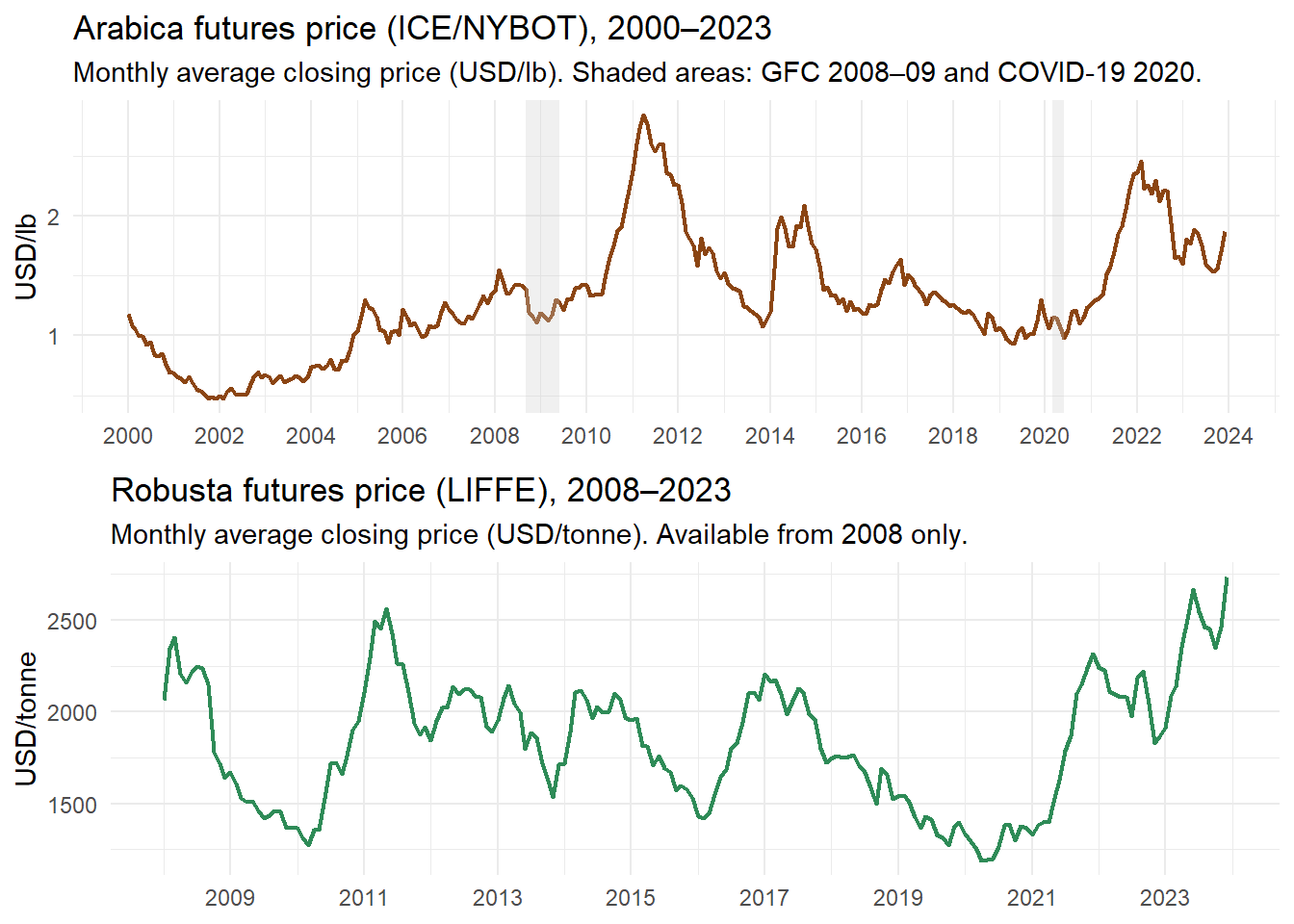

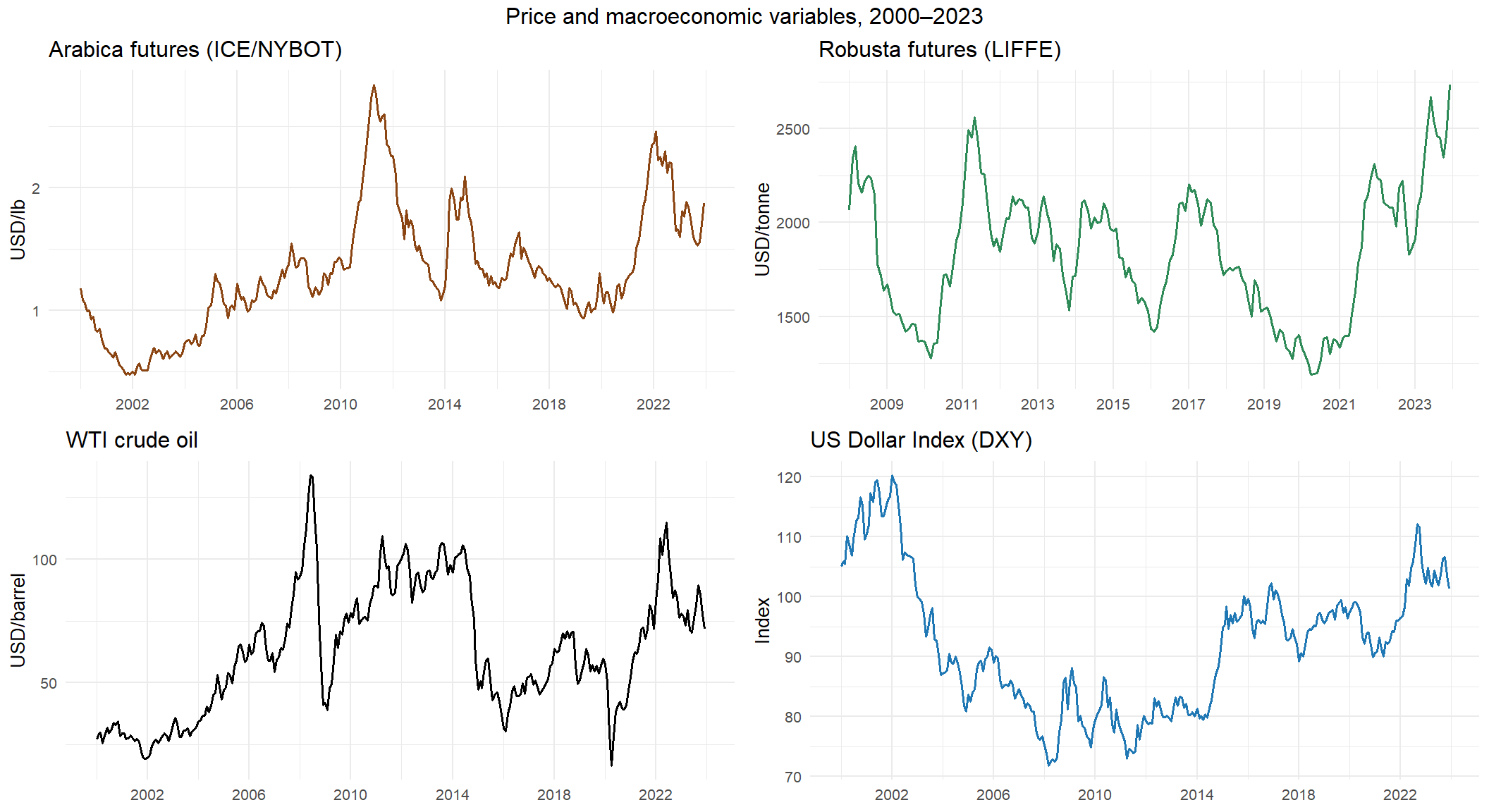

## Dependent Variables: Coffee Futures Prices

The two dependent variables are the monthly average closing prices of Arabica coffee futures traded on the ICE Futures U.S. exchange (NYBOT, contract code KCc) and Robusta coffee futures traded on the London International Financial Futures Exchange (LIFFE, contract code RCc). Both series are extracted from Refinitiv Eikon via the CEDIF data facility at UNIL, which constitutes the primary source for price data in this study. Arabica and Robusta are treated as two distinct dependent variables and modelled separately throughout the analysis, reflecting their different market structures, consumer bases and price determinants. A combined coffee price index is not constructed, as aggregation would obscure the variety-specific dynamics that this study aims to capture.

Daily closing prices are aggregated to monthly frequency by computing the arithmetic mean of all trading days within each calendar month. This averaging approach is preferred to using the last trading day's price because it is less sensitive to end-of-month volatility spikes associated with contract rollovers, and more representative of the price environment faced by market participants throughout the month.

The use of Refinitiv Eikon as the primary source for futures price data ensures institutional-grade data quality, with prices reflecting actual transaction records from the ICE and LIFFE exchanges rather than aggregated or estimated values from secondary sources.

This chunk reads the four Refinitiv price series — Arabica, Robusta, Cocoa and Sugar — from their raw Excel files and aggregates them from daily to monthly frequency. A single reusable function handles the parsing logic for all four files, which share the same Refinitiv export format. The chunk then builds the time series plots for the two dependent variables.

```{r prix_arabica_robusta, message = FALSE}

# ----------------------------------------------------------

# READING FUNCTION — REFINITIV EXCEL FORMAT

# Refinitiv exports contain metadata rows above the actual

# data. The function locates the header row by searching for

# the string "Exchange Date" in the first column, discards

# everything above it, converts the raw Excel date serial

# numbers to proper R Date objects, and aggregates daily

# closing prices to monthly averages.

#

# Arguments:

# fichier : path to the .xlsx file

# nom_variable : name to assign to the price column

# in the returned data frame

# Returns:

# A two-column data frame: date (YYYY-MM) and the named

# monthly average price variable.

# ----------------------------------------------------------

lire_refinitiv <- function(fichier, nom_variable) {

# Read the raw file without column names (metadata rows present)

df_raw <- read_excel(fichier, col_names = FALSE)

# Locate the header row containing "Exchange Date"

idx_hdr <- which(sapply(df_raw[[1]], function(x)

identical(as.character(x), "Exchange Date")))

if (length(idx_hdr) == 0) stop("Header not found in: ", fichier)

# Retain only the two relevant columns (date and close price)

# starting from the row immediately after the header

df_data <- df_raw[(idx_hdr + 1):nrow(df_raw), 1:2]

colnames(df_data) <- c("date_raw", "close")

df_data %>%

mutate(

# Refinitiv stores dates as Excel serial numbers (days since

# 1899-12-30). Multiply by 86400 to convert to POSIX seconds.

date_raw = as.Date(as.POSIXct(as.numeric(date_raw) * 86400,

origin = "1899-12-30", tz = "UTC")),

close = as.numeric(close)

) %>%

filter(!is.na(date_raw), !is.na(close)) %>%

arrange(date_raw) %>%

# Aggregate to monthly frequency: compute the arithmetic mean

# of all trading days within each calendar month.

# This is preferred over end-of-month prices as it is less

# sensitive to contract rollover volatility.

mutate(date = format(date_raw, "%Y-%m")) %>%

group_by(date) %>%

summarise(!!nom_variable := mean(close, na.rm = TRUE), .groups = "drop")

}

# Apply the function to all four Refinitiv price series

arabica <- lire_refinitiv(FICHIER_ARABICA, "prix_arabica")

robusta <- lire_refinitiv(FICHIER_ROBUSTA, "prix_robusta")

cacao_ny <- lire_refinitiv(FICHIER_CACAO_NY, "prix_cacao")

sucre_11 <- lire_refinitiv(FICHIER_SUCRE_11, "prix_sucre")

# ----------------------------------------------------------

# PLOT DATA — DEPENDENT VARIABLES

# Build a complete monthly date spine covering the full

# analysis period, then left-join the two coffee price

# series. Left-joining preserves all months in the spine,

# so months with no Robusta data (2000-2007) appear as NA

# rather than being silently dropped.

# ----------------------------------------------------------

df_prix <- data.frame(

date = format(seq(as.Date("2000-01-01"),

as.Date("2023-12-01"), by = "month"), "%Y-%m")

) %>%

left_join(arabica, by = "date") %>%

left_join(robusta, by = "date") %>%

mutate(date_fmt = as.Date(paste0(date, "-01")))

# ----------------------------------------------------------

# PLOT 1 — ARABICA FUTURES PRICE (2000-2023)

# Shaded rectangles highlight two major macroeconomic shocks:

# the Global Financial Crisis (Sep 2008 - Jun 2009) and the

# first wave of COVID-19 (Mar - Jun 2020).

# ----------------------------------------------------------

p1 <- ggplot(df_prix, aes(x = date_fmt, y = prix_arabica)) +

geom_line(color = "#8B4513", linewidth = 0.8) +

annotate("rect",

xmin = as.Date("2008-09-01"), xmax = as.Date("2009-06-01"),

ymin = -Inf, ymax = Inf,

fill = "grey80", alpha = 0.3) +

annotate("rect",

xmin = as.Date("2020-03-01"), xmax = as.Date("2020-06-01"),

ymin = -Inf, ymax = Inf,

fill = "grey80", alpha = 0.3) +

labs(title = "Arabica futures price (ICE/NYBOT), 2000–2023",

subtitle = "Monthly average closing price (USD/lb). Shaded areas: GFC 2008–09 and COVID-19 2020.",

x = NULL, y = "USD/lb") +

theme_minimal(base_size = 11) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y")

# ----------------------------------------------------------

# PLOT 2 — ROBUSTA FUTURES PRICE (2008-2023)

# Rows with NA Robusta prices (2000-2007) are excluded before

# plotting to avoid a misleading gap at the left of the axis.

# ----------------------------------------------------------

p2 <- ggplot(filter(df_prix, !is.na(prix_robusta)),

aes(x = date_fmt, y = prix_robusta)) +

geom_line(color = "#2E8B57", linewidth = 0.8) +

labs(title = "Robusta futures price (LIFFE), 2008–2023",

subtitle = "Monthly average closing price (USD/tonne). Available from 2008 only.",

x = NULL, y = "USD/tonne") +

theme_minimal(base_size = 11) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y")

gridExtra::grid.arrange(p1, p2, ncol = 1)

```

The Arabica price series covers the full 2000–2023 period and exhibits the characteristic volatility of agricultural commodity markets, with a major price spike in 2010–2011 driven by supply shortfalls in Brazil and Colombia, and a renewed surge in 2021–2022 associated with adverse weather conditions and post-pandemic supply chain disruptions. The Robusta series, available from 2008, follows a broadly similar trajectory but at lower absolute price levels, reflecting its use primarily in soluble coffee and blends.

## Market Spillover Variables

Sugar and cocoa prices are included as potential spillover variables. Coffee, sugar and cocoa are all tropical agricultural commodities subject to similar climate shocks and traded on overlapping futures markets. Land substitution between coffee and sugar cultivation in Brazil — the world's largest producer of both — creates a supply-side linkage between the two markets. The Sugar No.11 contract (raw cane sugar, ICE Futures U.S.) and the ICE New York cocoa contract are used, both sourced from Refinitiv via CEDIF and aggregated to monthly frequency using the same procedure as the coffee price series.

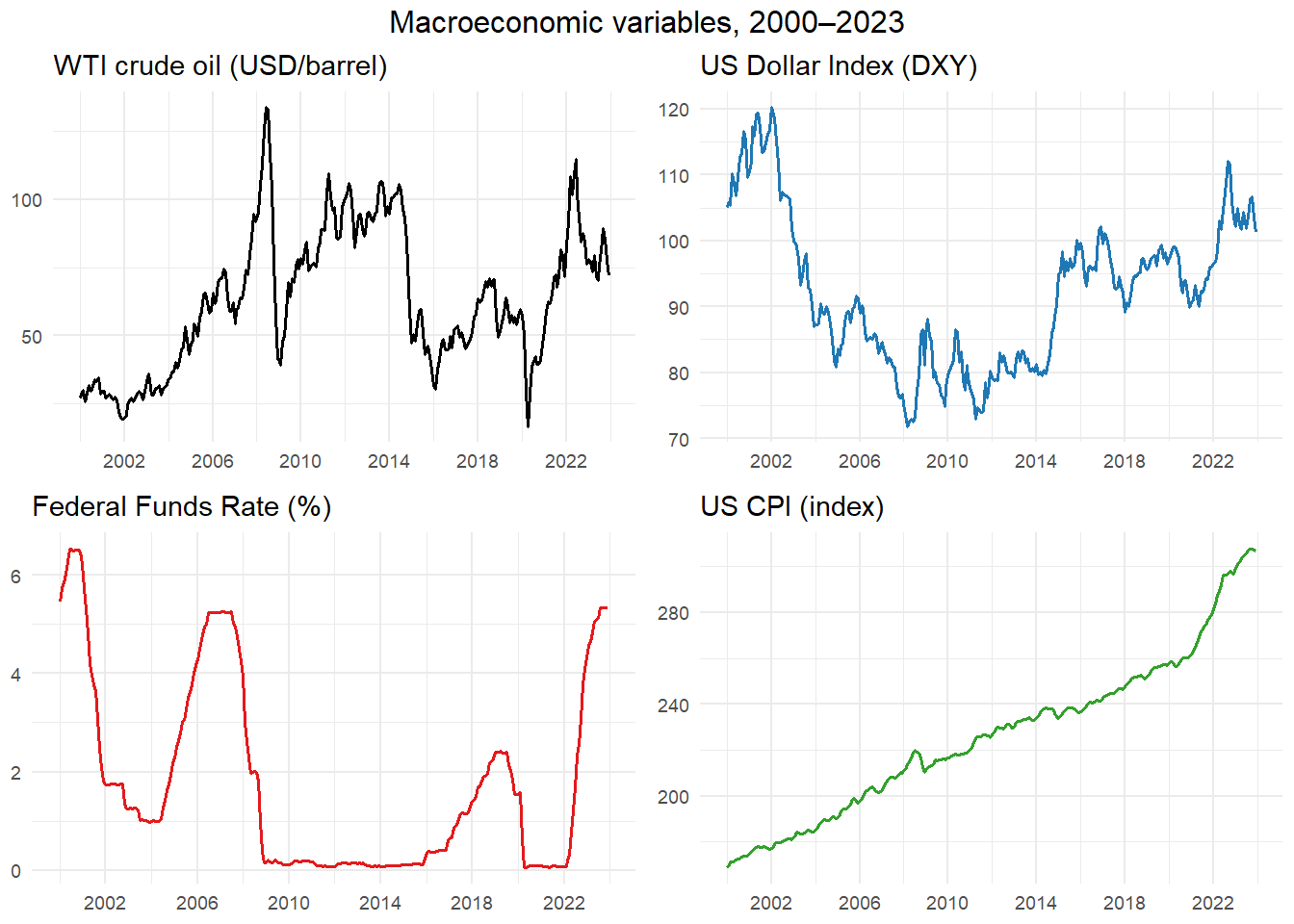

## Macroeconomic Variables

Four macroeconomic variables are included to capture the broader financial and monetary environment that influences commodity prices. All four are sourced from the Federal Reserve Economic Data (FRED) database maintained by the Federal Reserve Bank of St. Louis and are available at monthly frequency.

The WTI crude oil price captures the energy cost dimension of coffee production and transportation, as well as the broad commodity price cycle that tends to co-move across raw materials. The US Dollar Index (DXY), sourced from Investing.com, measures the value of the US dollar against a basket of major currencies; since coffee futures are denominated in US dollars, a stronger dollar tends to depress prices for non-dollar buyers, reducing global demand. The Federal Funds Rate proxies the monetary policy stance of the Federal Reserve, which influences global capital flows, risk appetite and commodity price dynamics. The Consumer Price Index (CPI) captures the general inflation environment.

This chunk reads the four macroeconomic variables from their respective source files and produces a four-panel time series plot. Three series — CPI, WTI and the Federal Funds Rate — are downloaded from FRED and share an identical CSV structure, handled by a single reusable function. The Dollar Index (DXY) requires separate parsing because its Investing.com export uses a different date format and embeds numeric commas in price values.

```{r macro}

# ----------------------------------------------------------

# READING FUNCTION — FRED CSV FORMAT

# FRED exports are two-column CSVs with a date column and

# a value column. The function renames both columns, converts

# the date to YYYY-MM format, and returns a two-column frame

# ready for joining against the monthly date spine.

#

# Arguments:

# fichier : path to the .csv file

# nom_variable : name to assign to the value column

# ----------------------------------------------------------

lire_fred <- function(fichier, nom_variable) {

df <- read_csv(fichier, show_col_types = FALSE)

colnames(df) <- c("date_raw", nom_variable)

df %>%

mutate(date = format(as.Date(date_raw), "%Y-%m")) %>%

select(date, all_of(nom_variable))

}

# Apply to the three FRED series

cpi <- lire_fred(FICHIER_CPI, "cpi")

wti <- lire_fred(FICHIER_WTI, "wti")

fed <- lire_fred(FICHIER_FED, "fed_funds_rate")

# ----------------------------------------------------------

# DXY — INVESTING.COM FORMAT (REQUIRES SEPARATE PARSING)

# The Investing.com CSV uses a non-standard date format

# (MM/DD/YYYY), wraps all fields in double quotes, and

# formats numeric values with comma thousands separators

# (e.g. "1,234.56"). Standard read_csv() fails on this

# structure, so the file is read line by line, quotes are

# stripped manually, and commas inside numbers are removed

# before coercing to numeric.

# ----------------------------------------------------------

dxy_lines <- readLines(FICHIER_DXY)

# Remove all double-quote characters from every line

dxy_clean <- gsub('"', '', dxy_lines)

# Re-parse the cleaned text as a standard CSV

dxy_df <- read.csv(text = paste(dxy_clean, collapse = "\n"),

stringsAsFactors = FALSE)

dxy <- dxy_df %>%

select(date_raw = 1, dxy = 2) %>%

mutate(

# Remove thousands separator commas before coercing to numeric

dxy = as.numeric(gsub(",", "", as.character(dxy))),

# Convert MM/DD/YYYY date strings to YYYY-MM format

date = format(as.Date(date_raw, format = "%m/%d/%Y"), "%Y-%m")

) %>%

filter(!is.na(date), !is.na(dxy)) %>%

arrange(date) %>%

select(date, dxy)

# ----------------------------------------------------------

# PLOT DATA — MACROECONOMIC VARIABLES

# A complete monthly date spine is built for 2000-2023, then

# all four series are left-joined onto it. Left-joining

# ensures that any months missing from individual series

# appear as NA rather than collapsing the spine.

# ----------------------------------------------------------

df_macro <- data.frame(

date = format(seq(as.Date("2000-01-01"),

as.Date("2023-12-01"), by = "month"), "%Y-%m")

) %>%

left_join(wti, by = "date") %>%

left_join(dxy, by = "date") %>%

left_join(fed, by = "date") %>%

left_join(cpi, by = "date") %>%

mutate(date_fmt = as.Date(paste0(date, "-01")))

# ----------------------------------------------------------

# FOUR-PANEL TIME SERIES PLOT

# Each panel uses a distinct color to differentiate the

# series at a glance. No y-axis label is added since the

# panel title already carries the unit information.

# ----------------------------------------------------------

gridExtra::grid.arrange(

ggplot(df_macro, aes(date_fmt, wti)) +

geom_line(color = "black", linewidth = 0.6) +

labs(title = "WTI crude oil (USD/barrel)", x = NULL, y = NULL) +

theme_minimal(base_size = 9) +

scale_x_date(date_breaks = "4 years", date_labels = "%Y"),

ggplot(df_macro, aes(date_fmt, dxy)) +

geom_line(color = "#1f78b4", linewidth = 0.6) +

labs(title = "US Dollar Index (DXY)", x = NULL, y = NULL) +

theme_minimal(base_size = 9) +

scale_x_date(date_breaks = "4 years", date_labels = "%Y"),

ggplot(df_macro, aes(date_fmt, fed_funds_rate)) +

geom_line(color = "#e31a1c", linewidth = 0.6) +

labs(title = "Federal Funds Rate (%)", x = NULL, y = NULL) +

theme_minimal(base_size = 9) +

scale_x_date(date_breaks = "4 years", date_labels = "%Y"),

ggplot(df_macro, aes(date_fmt, cpi)) +

geom_line(color = "#33a02c", linewidth = 0.6) +

labs(title = "US CPI (index)", x = NULL, y = NULL) +

theme_minimal(base_size = 9) +

scale_x_date(date_breaks = "4 years", date_labels = "%Y"),

ncol = 2,

top = "Macroeconomic variables, 2000–2023"

)

write.csv(cpi, file.path(PATH_OUTPUT, "cpi.csv"), row.names = FALSE)

write.csv(wti, file.path(PATH_OUTPUT, "wti.csv"), row.names = FALSE)

write.csv(fed, file.path(PATH_OUTPUT, "fed.csv"), row.names = FALSE)

write.csv(dxy, file.path(PATH_OUTPUT, "dxy.csv"), row.names = FALSE)

```

For models estimated at quarterly frequency — specifically those incorporating OECD GDP growth — all monthly macroeconomic variables are aggregated to quarterly frequency by computing the mean of the three constituent months. The OECD quarterly real GDP growth rate (growth rate period-on-period) is sourced from the OECD Data Explorer and covers the 38 OECD member countries, which collectively represent the principal coffee-consuming economies. This variable captures the demand-side dynamics of the global coffee market: when economic activity accelerates in OECD countries, per-capita coffee consumption tends to increase, exerting upward pressure on prices.

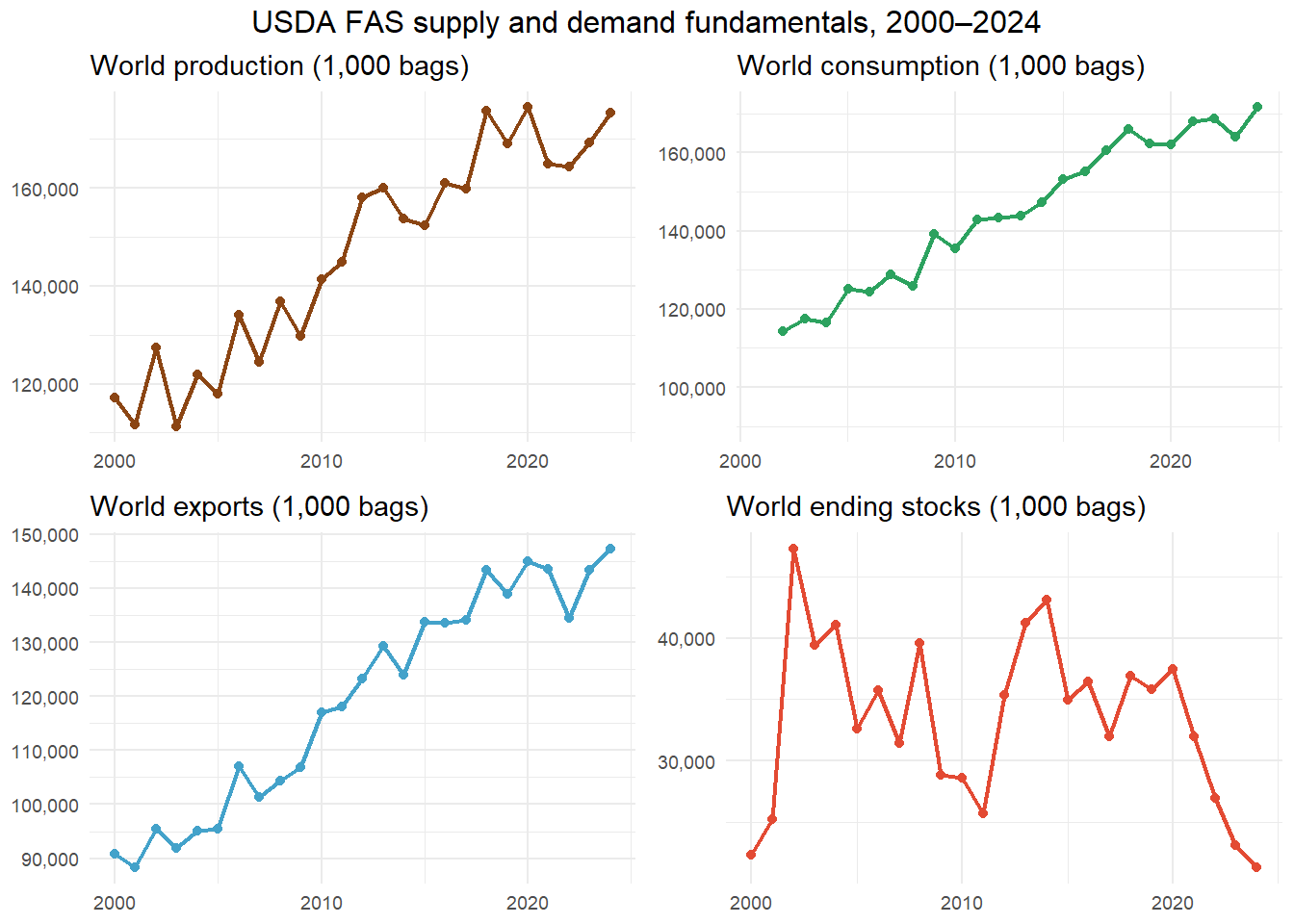

## Market Fundamentals: USDA Production, Supply and Distribution

Supply-and-demand fundamentals are sourced from the USDA Foreign Agricultural Service Production, Supply and Distribution (PSD) Online database, which publishes annual crop-year estimates for over 190 countries across all major agricultural commodities. Four variables are retained: world coffee production, world domestic consumption, world exports and world ending stocks. These are aggregated to world totals by summing across all countries for each crop year.

This chunk reads the USDA FAS PSD export file, aggregates country-level data to world totals for the four supply-and-demand variables, and expands the resulting annual series to monthly frequency by repeating each crop-year value across the twelve months of that year. The raw file uses an unusual structure — a single-column CSV embedded inside an Excel file — which requires a two-step parsing approach before standard tidyverse operations can be applied.

```{r usda, message=FALSE, warning=FALSE}

# ----------------------------------------------------------

# STEP 1 — PARSE THE RAW USDA FILE

# The USDA FAS PSD export is structured as an Excel file

# whose first column contains a single long CSV string, with

# the header in row 1 and one data record per subsequent row.

# The file is first read as a raw Excel object, then the

# embedded CSV is reconstructed and parsed properly.

# ----------------------------------------------------------

df_usda_raw <- read_excel(FICHIER_USDA, col_names = FALSE)

# Extract the header string from cell [1,1]

col_name <- as.character(df_usda_raw[1, 1])

# Extract all non-empty data rows from column 1

lignes <- df_usda_raw[-1, 1] %>%

pull() %>%

na.omit() %>%

as.character()

# Reassemble and parse as a standard CSV

df_usda <- read_csv(I(paste(c(col_name, lignes), collapse = "\n")),

show_col_types = FALSE)

# ----------------------------------------------------------

# STEP 2 — AGGREGATE TO WORLD TOTALS

# The PSD database contains one row per country per crop year

# per attribute. Summing across all countries yields world

# totals for the four variables of interest.

# Consumption for crop year 2000 is set to NA due to

# incomplete EU reporting in the PSD for that year.

# ----------------------------------------------------------

df_usda_world <- df_usda %>%

filter(Attribute_Description %in% c("Production", "Domestic Consumption",

"Exports", "Ending Stocks"),

Market_Year >= 2000, Market_Year <= 2024) %>%

group_by(Market_Year, Attribute_Description) %>%

summarise(valeur = sum(Value, na.rm = TRUE), .groups = "drop") %>%

# Reshape from long to wide: one column per supply-demand variable

pivot_wider(names_from = Attribute_Description, values_from = valeur) %>%

rename(annee = Market_Year,

production = Production,

consommation = `Domestic Consumption`,

exportations = Exports,

ending_stocks = `Ending Stocks`) %>%

arrange(annee) %>%

# Flag year-2000 consumption as missing (incomplete source data)

mutate(consommation = ifelse(annee == 2000, NA, consommation))

# ----------------------------------------------------------

# STEP 3 — EXPAND TO MONTHLY FREQUENCY

# USDA data are published at annual crop-year frequency.

# Each year's value is repeated across the 12 calendar months

# of that year, reflecting the assumption that market

# participants incorporate annual supply-demand estimates

# into pricing decisions throughout the crop year.

# ----------------------------------------------------------

df_usda_monthly <- df_usda_world %>%

rowwise() %>%

do({

annee <- .$annee

data.frame(

date = format(seq(as.Date(paste0(annee, "-01-01")),

as.Date(paste0(annee, "-12-01")),

by = "month"), "%Y-%m"),

production = .$production,

consommation = .$consommation,

exportations = .$exportations,

ending_stocks = .$ending_stocks

)

}) %>%

ungroup()

# ----------------------------------------------------------

# STEP 4 — FOUR-PANEL PLOT OF ANNUAL WORLD TOTALS

# The plot uses the annual (non-expanded) data for clarity.

# Each point represents one crop year. Consumption starts

# at 2001 to avoid plotting the documented NA for 2000.

# A minimum y-axis floor of 90,000 is applied to consumption

# to prevent the axis from starting at zero and compressing

# the visible variation in the series.

# ----------------------------------------------------------

df_usda_plot <- df_usda_world %>%

mutate(date_fmt = as.Date(paste0(annee, "-01-01")))

gridExtra::grid.arrange(

ggplot(df_usda_plot, aes(date_fmt, production)) +

geom_line(color = "#8B4513", linewidth = 0.8, na.rm = TRUE) +

geom_point(size = 1.5, color = "#8B4513", na.rm = TRUE) +

scale_y_continuous(labels = scales::comma) +

labs(title = "World production (1,000 bags)", x = NULL, y = NULL) +

theme_minimal(base_size = 9),

# Filter out 2000 NA so the consumption chart starts cleanly at 2001

ggplot(filter(df_usda_plot, !is.na(consommation)),

aes(date_fmt, consommation)) +

geom_line(color = "#2ca25f", linewidth = 0.8) +

geom_point(size = 1.5, color = "#2ca25f") +

scale_y_continuous(labels = scales::comma, limits = c(90000, NA)) +

labs(title = "World consumption (1,000 bags)", x = NULL, y = NULL) +

theme_minimal(base_size = 9),

ggplot(df_usda_plot, aes(date_fmt, exportations)) +

geom_line(color = "#43a2ca", linewidth = 0.8, na.rm = TRUE) +

geom_point(size = 1.5, color = "#43a2ca", na.rm = TRUE) +

scale_y_continuous(labels = scales::comma) +

labs(title = "World exports (1,000 bags)", x = NULL, y = NULL) +

theme_minimal(base_size = 9),

ggplot(df_usda_plot, aes(date_fmt, ending_stocks)) +

geom_line(color = "#e34a33", linewidth = 0.8, na.rm = TRUE) +

geom_point(size = 1.5, color = "#e34a33", na.rm = TRUE) +

scale_y_continuous(labels = scales::comma) +

labs(title = "World ending stocks (1,000 bags)", x = NULL, y = NULL) +

theme_minimal(base_size = 9),

ncol = 2,

top = "USDA FAS supply and demand fundamentals, 2000–2024"

)

```

Since USDA data are published at annual (crop-year) frequency, they are expanded to monthly frequency by repeating each year's value across the 12 calendar months of that year. This approach assumes that market participants incorporate supply-demand fundamentals into their pricing decisions throughout the entire crop year. While the USDA releases monthly updates to its World Agricultural Supply and Demand Estimates (WASDE), the annual PSD figures used here represent end-of-year consolidated estimates. Repeating the annual value across twelve months is a standard simplification when monthly supply-demand data are unavailable.

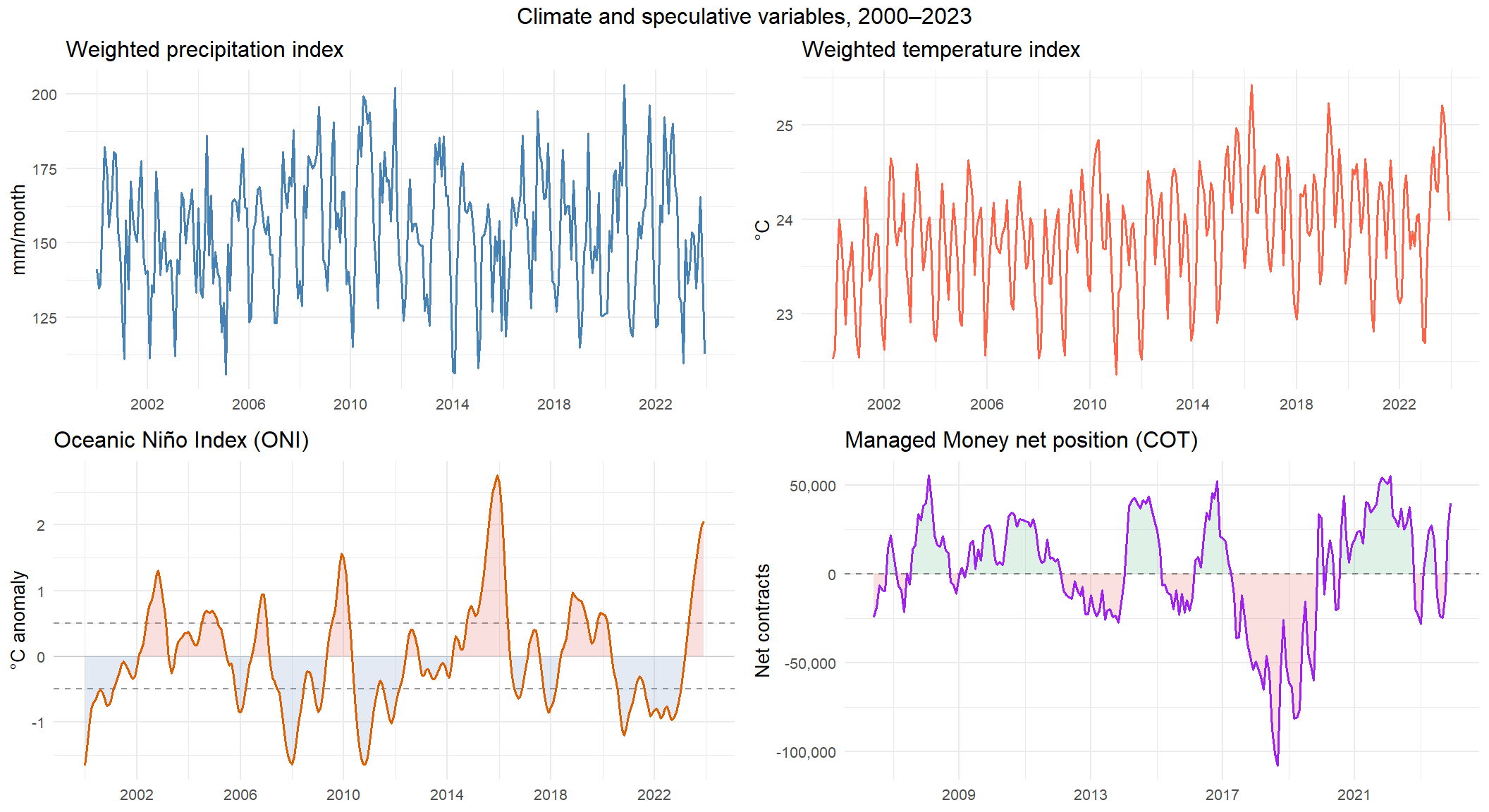

## Climate Variables

### Selection of Producer Countries

Climate conditions in coffee-producing regions directly affect supply through their impact on cherry development, flowering and yield. Temperature and precipitation are the two primary climatic determinants of coffee production at the agronomy level. Rather than using a single country or global average, this study constructs weighted climate indices that aggregate conditions across the 14 countries that account for the largest share of world coffee production.

The selection of these 14 countries follows a systematic, data-driven criterion: only countries whose average annual share of world coffee production exceeds 1% over the 2000–2024 period are included. This threshold is computed directly from the USDA FAS PSD data used for the supply fundamentals variables, ensuring full consistency between the production weights and the underlying data source. The table below reports the calculated production shares and confirms the selection criterion.

This chunk derives the country selection criterion for the climate indices directly from the USDA PSD data already loaded in the previous chunk. For each crop year, each country's share of world production is computed, and the 25-year average of that share is then calculated across the full 2000–2024 period. Only countries whose average share meets or exceeds the 1% threshold are retained. Using the same USDA source as the fundamentals variables ensures full consistency between the production weights and the underlying data.

```{r selection_pays, echo=TRUE}

# ----------------------------------------------------------

# STEP 1 — COMPUTE ANNUAL PRODUCTION SHARES BY COUNTRY

# For each crop year, world total production is computed

# first as a denominator, then each country's share is

# expressed as a percentage of that total.

# ----------------------------------------------------------

prod_by_country <- df_usda %>%

filter(Attribute_Description == "Production",

Market_Year >= 2000, Market_Year <= 2024) %>%

group_by(Market_Year) %>%

# Compute world total for the denominator within each year

mutate(world_total = sum(Value, na.rm = TRUE)) %>%

ungroup() %>%

# Each country's share as a percentage of world production

mutate(share_pct = Value / world_total * 100) %>%

# ----------------------------------------------------------

# STEP 2 — AVERAGE SHARE OVER 2000-2024 AND APPLY THRESHOLD

# Averaging over 25 years smooths out year-to-year production

# fluctuations caused by weather or disease, yielding stable

# structural weights that reflect each country's long-run

# contribution to global supply.

# The 1% threshold is applied to exclude countries whose

# individual contribution is too small to have a meaningful

# impact on the aggregated climate indices.

# ----------------------------------------------------------

group_by(Country_Name) %>%

summarise(avg_share = round(mean(share_pct, na.rm = TRUE), 2),

.groups = "drop") %>%

arrange(desc(avg_share)) %>%

filter(avg_share >= 1.0) %>%

# Correct encoding of Côte d'Ivoire (stored without accent in USDA PSD)

mutate(Country_Name = recode(Country_Name,

"Cote d'Ivoire" = "Côte d'Ivoire"))

# ----------------------------------------------------------

# STEP 3 — DISPLAY THE SELECTION TABLE

# The caption dynamically computes the combined production

# share of the selected countries, confirming that the 14

# retained countries collectively represent ~90.8% of world

# production over the analysis period.

# ----------------------------------------------------------

kable(prod_by_country,

caption = paste0("Countries with average annual production share ≥ 1%, ",

"2000–2024 (USDA FAS PSD). ",

"Total: ", round(sum(prod_by_country$avg_share), 1), "%."),

col.names = c("Country", "Avg. share (%)"),

booktabs = TRUE) %>%

kable_styling(bootstrap_options = c("striped", "hover"),

font_size = 11, full_width = FALSE)

```

This chunk converts the raw production shares computed in the previous chunk into normalised weights that sum exactly to one. These weights are the core of the climate index construction: every weighted average in the subsequent climate chunks is computed using `POIDS_PRODUCTION`. Two parallel vectors map official country names as they appear in the USDA PSD database to the internal identifiers used in the file lists defined in the setup chunk, ensuring that the correct weight is always matched to the correct file.

```{r poids_production}

# ----------------------------------------------------------

# STEP 1 — DEFINE THE NAME MAPPING BETWEEN USDA AND FILES

# The USDA PSD database uses official English country names,

# while the climate file lists (FICHIERS_PRECIP, FICHIERS_TEMP)

# use shorter internal identifiers without accents, defined

# in the setup chunk. The two vectors below establish the

# one-to-one correspondence between the two naming systems.

# The order in both vectors must be identical.

# ----------------------------------------------------------

pays_retenus <- c("Brazil", "Vietnam", "Colombia", "Indonesia", "Ethiopia",

"India", "Honduras", "Mexico", "Uganda", "Guatemala",

"Peru", "Côte d'Ivoire", "Nicaragua", "Costa Rica")

noms_internes <- c("bresil", "vietnam", "colombie", "indonesie", "ethiopie",

"inde", "honduras", "mexique", "uganda", "guatemala",

"perou", "cote_ivoire", "nicaragua", "costa_rica")

# ----------------------------------------------------------

# STEP 2 — BUILD THE RAW PRODUCTION SHARE VECTOR

# match() looks up each country name from prod_by_country

# in pays_retenus and returns its position, which is then

# used to retrieve the corresponding internal identifier.

# setNames() attaches those identifiers as vector names,

# so that PARTS_PRODUCTION["bresil"] returns Brazil's share.

# ----------------------------------------------------------

PARTS_PRODUCTION <- setNames(

prod_by_country$avg_share,

noms_internes[match(prod_by_country$Country_Name, pays_retenus)]

)

# ----------------------------------------------------------

# STEP 3 — NORMALISE TO UNIT SUM (PRODUCTION WEIGHTS)

# Dividing by the total ensures the weights sum exactly to 1,

# as required by the weighted index formula. This normalisation

# step is necessary because the 14 selected countries do not

# collectively account for 100% of world production — the

# remaining ~9% belongs to countries below the 1% threshold.

# ----------------------------------------------------------

POIDS_PRODUCTION <- PARTS_PRODUCTION / sum(PARTS_PRODUCTION)

# ----------------------------------------------------------

# VERIFICATION

# Confirms that all 14 internal names were matched correctly

# and that no NA values were introduced by the name mapping.

# Any NA in the output would indicate a mismatch between

# pays_retenus and the country names in prod_by_country.

# ----------------------------------------------------------

cat("Names of POIDS_PRODUCTION:", names(POIDS_PRODUCTION), "\n")

```

The 14 selected countries collectively account for `r round(sum(prod_by_country$avg_share), 1)`% of world coffee production on average over 2000–2024. Countries falling below the 1% threshold have a negligible and individually undifferentiated impact on global supply, and their inclusion would add noise without improving the explanatory power of the climate indices.

Before constructing variety-specific production weights, the share of Arabica and Robusta production is computed for each of the 14 retained countries directly from the USDA FAS PSD data. The `Arabica Production` and `Robusta Production` attributes are available as separate line items in the raw dataset, allowing the variety split to be calculated empirically rather than assumed from external sources. This ensures full consistency with the data already used for the global production weights. The table below reports the calculated variety shares for each of the 14 countries over the 2000–2024 period.

```{r variety_splits, echo=TRUE}

# ----------------------------------------------------------

# VARIETY SPLITS — ARABICA VS ROBUSTA PER COUNTRY

# The USDA FAS PSD dataset contains separate line items for

# "Arabica Production" and "Robusta Production" per country.

# Summing across 2000-2024 and computing shares yields the

# empirical variety split for each of the 14 retained countries.

# These splits are used downstream to assign each country

# to the correct variety-specific climate index.

# The recode of Cote d'Ivoire is applied BEFORE the filter

# to ensure the country is correctly matched to pays_retenus.

# ----------------------------------------------------------

splits_variete <- df_usda %>%

filter(Attribute_Description %in% c("Arabica Production",

"Robusta Production"),

Market_Year >= 2000, Market_Year <= 2024) %>%

group_by(Country_Name, Attribute_Description) %>%

summarise(total = sum(Value, na.rm = TRUE), .groups = "drop") %>%

pivot_wider(names_from = Attribute_Description,

values_from = total,

values_fill = 0) %>%

rename(arabica = `Arabica Production`,

robusta = `Robusta Production`) %>%

mutate(

Country_Name = recode(Country_Name,

"Cote d'Ivoire" = "Côte d'Ivoire"),

total = arabica + robusta,

pct_arabica = round(arabica / total * 100, 1),

pct_robusta = round(robusta / total * 100, 1)

) %>%

filter(Country_Name %in% pays_retenus) %>%

arrange(desc(total))

kable(splits_variete %>% select(Country_Name, arabica, robusta,

total, pct_arabica, pct_robusta),

caption = "Variety splits — Arabica vs Robusta production share per country (2000–2024, USDA FAS PSD)",

booktabs = TRUE,

col.names = c("Country", "Arabica (1000 bags)",

"Robusta (1000 bags)", "Total",

"% Arabica", "% Robusta")) %>%

kable_styling(bootstrap_options = c("striped", "hover"),

font_size = 11, full_width = TRUE)

```

The variety split table confirms the expected production geography of the two coffee varieties. Nine countries produce exclusively or quasi-exclusively Arabica — Colombia, Ethiopia, Honduras, Peru, Costa Rica, Guatemala, Nicaragua and Mexico all report Arabica shares above 90%, and are therefore assigned entirely to the Arabica group. Brazil, the world's largest producer, is the only major country with a significant mixed production, reporting 72.3% Arabica and 27.7% Robusta over the 2000–2024 period. On the Robusta side, Vietnam and Côte d'Ivoire are quasi-pure Robusta producers at 96.8% and 100% respectively, while Indonesia (87.7%), Uganda (80.9%) and India (67.8%) produce predominantly but not exclusively Robusta.

Four countries contribute to both variety-specific indices: Brazil, India, Uganda and Indonesia. For these countries, the production weight assigned to each group is scaled by the empirically computed variety share rather than assumed from external sources. Countries with a variety share above 90% are treated as pure producers and assigned entirely to their dominant group — a simplification justified by the negligible contribution of the minority variety to their total output. This variety-aware weighting scheme ensures that the climate indices used in each model specification reflect conditions in the actual producing zones for that variety, rather than averaging over climatically relevant and irrelevant regions indiscriminately.

The variety-specific production weights are now constructed for each group. For the Arabica group, the nine producing countries are assigned weights proportional to their Arabica production share, adjusted by the empirically computed variety splits for mixed producers. The resulting weights sum to one and reflect the long-run structural contribution of each country to global Arabica supply over 2000–2024.

```{r poids_arabica}

# ----------------------------------------------------------

# VARIETY-SPECIFIC PRODUCTION WEIGHTS — ARABICA GROUP

# Countries assigned to the Arabica group and their variety

# splits (from splits_variete). Countries with >90% Arabica

# share are treated as pure producers (split = 1.0).

# Mixed producers (Brazil, India, Uganda, Indonesia) receive

# their empirically computed Arabica share as a scaling factor.

# ----------------------------------------------------------

# Variety splits for Arabica group

# Pure producers (>90%) get 1.0, mixed producers get actual share

split_arabica <- c(

bresil = 0.723,

colombie = 1.000,

ethiopie = 1.000,

inde = 0.322,

honduras = 1.000,

mexique = 1.000,

guatemala = 1.000,

perou = 1.000,

nicaragua = 1.000,

costa_rica = 1.000

)

# Extract raw production shares for Arabica countries

# Uganda, Vietnam, Indonesia, Cote d'Ivoire are excluded

# as they are assigned to the Robusta group

noms_arabica <- names(split_arabica)

PARTS_ARABICA_RAW <- PARTS_PRODUCTION[

names(PARTS_PRODUCTION) %in% noms_arabica

]

# Apply variety split to adjust for mixed producers

PARTS_ARABICA_ADJ <- PARTS_ARABICA_RAW *

split_arabica[names(PARTS_ARABICA_RAW)]

# Normalise to unit sum

POIDS_ARABICA <- PARTS_ARABICA_ADJ / sum(PARTS_ARABICA_ADJ,

na.rm = TRUE)

# Display verification table

df_poids_arabica <- data.frame(

Country = names(POIDS_ARABICA),

Raw_share = round(PARTS_ARABICA_RAW[names(POIDS_ARABICA)], 4),

Split = round(split_arabica[names(POIDS_ARABICA)], 3),

Adj_share = round(PARTS_ARABICA_ADJ[names(POIDS_ARABICA)], 4),

Final_weight = round(POIDS_ARABICA, 4)

)

kable(df_poids_arabica,

caption = "Arabica production weights — variety-adjusted (2000–2024)",

booktabs = TRUE,

row.names = FALSE,

col.names = c("Country", "Raw share", "Arabica split",

"Adjusted share", "Final weight")) %>%

kable_styling(bootstrap_options = c("striped", "hover"),

font_size = 11, full_width = FALSE)

```

The same procedure is applied to the Robusta group. Five countries are assigned to this group — Vietnam, Indonesia, Uganda, Côte d'Ivoire and India — with variety splits applied to the four mixed producers. Vietnam and Côte d'Ivoire are treated as pure Robusta producers given their shares of 96.8% and 100% respectively.

```{r poids_robusta}

# ----------------------------------------------------------

# VARIETY-SPECIFIC PRODUCTION WEIGHTS — ROBUSTA GROUP

# Countries assigned to the Robusta group and their variety

# splits (from splits_variete). Vietnam and Cote d'Ivoire

# are treated as pure producers (split = 1.0).

# Mixed producers (Indonesia, Uganda, India, Brazil) receive

# their empirically computed Robusta share as a scaling factor.

# ----------------------------------------------------------

# Variety splits for Robusta group

split_robusta <- c(

vietnam = 1.000,

indonesie = 0.877,

uganda = 0.809,

cote_ivoire = 1.000,

inde = 0.678,

bresil = 0.277

)

# Extract raw production shares for Robusta countries

noms_robusta <- names(split_robusta)

PARTS_ROBUSTA_RAW <- PARTS_PRODUCTION[

names(PARTS_PRODUCTION) %in% noms_robusta

]

# Apply variety split to adjust for mixed producers

PARTS_ROBUSTA_ADJ <- PARTS_ROBUSTA_RAW *

split_robusta[names(PARTS_ROBUSTA_RAW)]

# Normalise to unit sum

POIDS_ROBUSTA <- PARTS_ROBUSTA_ADJ / sum(PARTS_ROBUSTA_ADJ,

na.rm = TRUE)

# Display verification table

df_poids_robusta <- data.frame(

Country = names(POIDS_ROBUSTA),

Raw_share = round(PARTS_ROBUSTA_RAW[names(POIDS_ROBUSTA)], 4),

Split = round(split_robusta[names(POIDS_ROBUSTA)], 3),

Adj_share = round(PARTS_ROBUSTA_ADJ[names(POIDS_ROBUSTA)], 4),

Final_weight = round(POIDS_ROBUSTA, 4)

)

kable(df_poids_robusta,

caption = "Robusta production weights — variety-adjusted (2000–2024)",

booktabs = TRUE,

row.names = FALSE,

col.names = c("Country", "Raw share", "Robusta split",

"Adjusted share", "Final weight")) %>%

kable_styling(bootstrap_options = c("striped", "hover"),

font_size = 11, full_width = FALSE)

```

### Climate Data Source and Spatial Resolution

Temperature and precipitation data are sourced from the World Bank Climate Knowledge Portal (CCKP), which provides access to the ERA5 reanalysis dataset produced by the European Centre for Medium-Range Weather Forecasts (ECMWF). ERA5 offers a spatial resolution of 0.25 degrees (approximately 28 km × 28 km at the equator), which is among the finest resolutions available for global gridded climate datasets covering the full 2000–2023 period.

Data are extracted at the Administrative Division Level 1 (ADM1) — that is, at the province or state level within each country. This sub-national resolution is preferred over country-level averages because coffee cultivation is highly concentrated within specific regions of each country. In Brazil, for instance, production is concentrated in Minas Gerais, São Paulo and Espírito Santo, while the Amazon basin produces virtually none. Using ADM1-level data allows the weighted climate indices to better reflect conditions in the actual producing zones, rather than averaging over climatically diverse national territories.

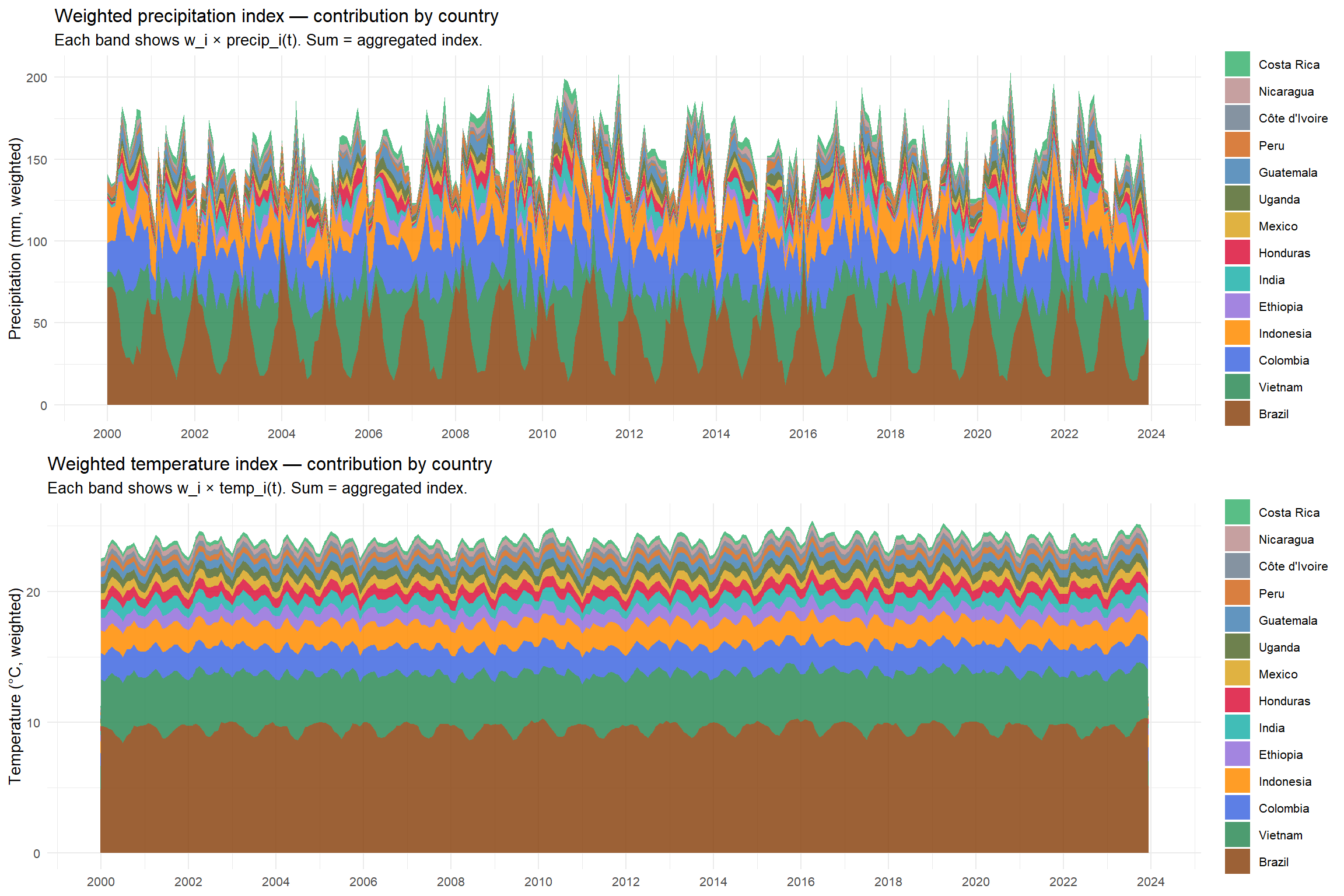

### Construction of the Weighted Climate Indices

For each of the 14 countries, a national monthly average is computed by taking the simple arithmetic mean across all ADM1 regions within the country. The weighted global index is then constructed as follows:

$$\text{Index}(t) = \sum_{i=1}^{14} w_i \cdot X_i(t)$$

where $X_i(t)$ is the national average value of the climate variable (precipitation in mm or temperature in °C) for country $i$ in month $t$, and $w_i$ is the normalised production weight of country $i$ (with $\sum w_i = 1$).

The production weights are held constant at their 2000–2024 averages rather than varying year by year. This fixed-weight approach is adopted to avoid a simultaneity problem: if a climate shock in year $t$ reduces production in a given country, its production share — and therefore its weight in the climate index — would be lower precisely in the year when the shock is most severe. Using time-varying weights would thus attenuate the very signal the index is designed to capture. Fixed weights computed over a long historical average naturally smooth out year-to-year fluctuations in production shares, avoiding the simultaneity bias that would arise from time-varying weights.

This chunk reads the ERA5 precipitation files for all 14 producer countries, computes a national monthly average across ADM1 regions within each country, and then aggregates the 14 national series into a single production-weighted global precipitation index. The reading logic is encapsulated in a reusable function that is applied to all 14 files simultaneously via `mapply()`. The resulting index is saved to disk for reuse in the final dataset assembly chunk.

```{r precipitations, message=FALSE}

# ----------------------------------------------------------

# READING FUNCTION — ERA5 ADM1 CLIMATE FILES

# Each ERA5 file contains one row per administrative region

# (ADM1) and one column per month, with a header row in row 1

# and two metadata columns ("code" and "name") that identify

# the region. The function strips the metadata columns,

# coerces all remaining values to numeric, and computes the

# simple arithmetic mean across all ADM1 regions within the

# country for each month. This yields a single national

# monthly average series per country.

#

# Arguments:

# fichier : path to the .xlsx file for one country

# nom_pays : internal country identifier (e.g. "bresil")

# variable : prefix for the output column ("precip" here)

#

# Returns:

# A two-column data frame: date (YYYY-MM) and the named

# national monthly average (e.g. "precip_bresil").

# ----------------------------------------------------------

lire_climat_pays <- function(fichier, nom_pays, variable = "precip") {

df_raw <- read_excel(fichier, col_names = FALSE)

# Promote the first row to column names

colnames(df_raw) <- as.character(df_raw[1, ])

df_raw <- df_raw[-1, ]

# Isolate the date columns by excluding the two metadata columns

cols_dates <- colnames(df_raw)[!colnames(df_raw) %in% c("code", "name")]

# Coerce all climate value columns to numeric

df_valeurs <- df_raw[, cols_dates] %>%

mutate(across(everything(), as.numeric))

# Average across all ADM1 regions (rows) for each month (column)

moyennes <- colMeans(df_valeurs, na.rm = TRUE)

# Return a tidy two-column data frame

df_pays <- data.frame(date = names(moyennes),

valeur = as.numeric(moyennes),

stringsAsFactors = FALSE)

colnames(df_pays)[2] <- paste0(variable, "_", nom_pays)

return(df_pays)

}

# ----------------------------------------------------------

# STEP 1 — READ ALL 14 COUNTRY FILES IN PARALLEL

# mapply() applies lire_climat_pays() to all 14 files at

# once, passing the file path and internal country name from

# FICHIERS_PRECIP simultaneously. The result is a named list

# of 14 two-column data frames, one per country.

# ----------------------------------------------------------

liste_precip <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_PRECIP,

nom_pays = names(FICHIERS_PRECIP),

variable = "precip",

SIMPLIFY = FALSE)

# ----------------------------------------------------------

# STEP 2 — MERGE INTO A SINGLE WIDE DATA FRAME

# Reduce() applies left_join() sequentially across the list,

# joining each country's series onto a growing wide frame

# keyed by date. The result has one row per month and one

# column per country (14 precipitation columns total).

# The frame is then filtered to the analysis period.

# ----------------------------------------------------------

df_precip_all <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_precip) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# ----------------------------------------------------------

# STEP 3 — COMPUTE THE PRODUCTION-WEIGHTED INDEX

# For each month, the weighted precipitation index is the

# dot product of the 14 national averages and POIDS_PRODUCTION.

# The column names are constructed to match the weight vector

# names exactly, ensuring the correct weight is applied to

# each country. rowwise() is used because c_across() requires

# operating on one row at a time.

#

# Index formula: indice_precip(t) = sum_i [ w_i * precip_i(t) ]

# where w_i are the fixed production weights summing to 1.

# ----------------------------------------------------------

cols_pays_precip <- paste0("precip_", names(POIDS_PRODUCTION))

df_precip_all <- df_precip_all %>%

rowwise() %>%

mutate(indice_precip = sum(c_across(all_of(cols_pays_precip)) * POIDS_PRODUCTION,

na.rm = TRUE)) %>%

ungroup()

# ----------------------------------------------------------

# STEP 4 — SAVE THE INDEX TO DISK

# Only the date and index columns are retained. The file is

# saved to the output folder and reloaded in the final

# dataset assembly chunk to avoid recomputing from scratch.

# ----------------------------------------------------------

df_indice_precip <- df_precip_all %>% select(date, indice_precip)

write.csv(df_indice_precip,

file.path(PATH_OUTPUT, "indice_precip_pondere_2000_2023.csv"),

row.names = FALSE)

write.csv(df_precip_all %>% select(date, starts_with("precip_")),

file.path(PATH_OUTPUT, "precip_disaggregated_2000_2023.csv"),

row.names = FALSE)

```

This chunk applies the exact same pipeline as the precipitation chunk to the temperature data. The `lire_climat_pays()` function defined previously is reused without modification — only the input file list, the variable prefix and the output filename change. The resulting production-weighted temperature index is saved to disk alongside the precipitation index.

```{r temperatures, message=FALSE}

# ----------------------------------------------------------

# STEP 1 — READ ALL 14 COUNTRY TEMPERATURE FILES

# Identical logic to the precipitation chunk: mapply() applies

# lire_climat_pays() to all 14 files in FICHIERS_TEMP,

# returning a named list of national monthly average series.

# The variable argument is set to "temp" so that output

# columns are named "temp_bresil", "temp_vietnam", etc.,

# matching the prefix expected when building cols_pays_temp.

# ----------------------------------------------------------

liste_temp <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_TEMP,

nom_pays = names(FICHIERS_TEMP),

variable = "temp",

SIMPLIFY = FALSE)

# ----------------------------------------------------------

# STEP 2 — MERGE AND FILTER TO THE ANALYSIS PERIOD

# Same Reduce/left_join pattern as for precipitation, yielding

# a wide frame with one temperature column per country and

# one row per month over 2000-2023.

# ----------------------------------------------------------

df_temp_all <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_temp) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# ----------------------------------------------------------

# STEP 3 — COMPUTE THE PRODUCTION-WEIGHTED TEMPERATURE INDEX

# The weighted index formula is identical to the precipitation

# case. Column names are prefixed with "temp_" to select the

# correct columns from the wide frame, and POIDS_PRODUCTION

# provides the same fixed weights used throughout.

#

# Index formula: indice_temp(t) = sum_i [ w_i * temp_i(t) ]

# where w_i are the fixed production weights summing to 1.

# ----------------------------------------------------------

cols_pays_temp <- paste0("temp_", names(POIDS_PRODUCTION))

df_temp_all <- df_temp_all %>%

rowwise() %>%

mutate(indice_temp = sum(c_across(all_of(cols_pays_temp)) * POIDS_PRODUCTION,

na.rm = TRUE)) %>%

ungroup()

# ----------------------------------------------------------

# STEP 4 — SAVE THE INDEX TO DISK

# As with precipitation, only the date and index columns are

# retained. The file is reloaded in the final assembly chunk.

# ----------------------------------------------------------

df_indice_temp <- df_temp_all %>% select(date, indice_temp)

write.csv(df_indice_temp,

file.path(PATH_OUTPUT, "indice_temp_pondere_2000_2023.csv"),

row.names = FALSE)

write.csv(df_temp_all %>% select(date, starts_with("temp_")),

file.path(PATH_OUTPUT, "temp_disaggregated_2000_2023.csv"),

row.names = FALSE)

```

The production-weighted climate indices constructed in the preceding sections aggregate temperature and precipitation conditions across all 14 producer countries regardless of the coffee variety they produce. As established in the variety split analysis, however, the production geographies of Arabica and Robusta are structurally distinct — Arabica is concentrated in Brazil, Colombia and Central America, while Robusta is dominated by Vietnam, Indonesia, Uganda and Côte d'Ivoire. Aggregating climate conditions across both groups in a single index dilutes the variety-specific signal: conditions in Vietnam are irrelevant to Arabica price formation, and conditions in Colombia are irrelevant to Robusta. Two variety-specific climate indices are therefore constructed using the variety-adjusted production weights derived above, one for each coffee group. The pipeline is identical to that used for the global indices — national ADM1 averages are computed and aggregated using the dot product of national values and variety-specific weights — with the difference that only the countries and weights relevant to each variety are included.

```{r indices_climatiques_arabica, message=FALSE}

# ----------------------------------------------------------

# VARIETY-SPECIFIC CLIMATE INDICES — ARABICA GROUP

# The same lire_climat_pays() function is reused without

# modification. Only the file lists and weight vectors change.

# Arabica group: Brazil, Colombia, Ethiopia, India, Honduras,

# Mexico, Guatemala, Peru, Nicaragua, Costa Rica.

# Mixed producers (Brazil, India) contribute their Arabica

# share only via POIDS_ARABICA.

# ----------------------------------------------------------

# STEP 1 — READ PRECIPITATION FILES FOR ARABICA COUNTRIES

FICHIERS_PRECIP_ARA <- FICHIERS_PRECIP[names(POIDS_ARABICA)]

liste_precip_ara <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_PRECIP_ARA,

nom_pays = names(FICHIERS_PRECIP_ARA),

variable = "precip",

SIMPLIFY = FALSE)

df_precip_ara <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_precip_ara) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# STEP 2 — COMPUTE WEIGHTED PRECIPITATION INDEX — ARABICA

cols_precip_ara <- paste0("precip_", names(POIDS_ARABICA))

df_precip_ara <- df_precip_ara %>%

rowwise() %>%

mutate(indice_precip_arabica = sum(

c_across(all_of(cols_precip_ara)) * POIDS_ARABICA,

na.rm = TRUE)) %>%

ungroup()

# STEP 3 — READ TEMPERATURE FILES FOR ARABICA COUNTRIES

FICHIERS_TEMP_ARA <- FICHIERS_TEMP[names(POIDS_ARABICA)]

liste_temp_ara <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_TEMP_ARA,

nom_pays = names(FICHIERS_TEMP_ARA),

variable = "temp",

SIMPLIFY = FALSE)

df_temp_ara <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_temp_ara) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# STEP 4 — COMPUTE WEIGHTED TEMPERATURE INDEX — ARABICA

cols_temp_ara <- paste0("temp_", names(POIDS_ARABICA))

df_temp_ara <- df_temp_ara %>%

rowwise() %>%

mutate(indice_temp_arabica = sum(

c_across(all_of(cols_temp_ara)) * POIDS_ARABICA,

na.rm = TRUE)) %>%

ungroup()

# STEP 5 — SAVE TO DISK

df_indice_precip_arabica <- df_precip_ara %>%

select(date, indice_precip_arabica)

df_indice_temp_arabica <- df_temp_ara %>%

select(date, indice_temp_arabica)

write.csv(df_indice_precip_arabica,

file.path(PATH_OUTPUT, "indice_precip_arabica_2000_2023.csv"),

row.names = FALSE)

write.csv(df_indice_temp_arabica,

file.path(PATH_OUTPUT, "indice_temp_arabica_2000_2023.csv"),

row.names = FALSE)

```

```{r indices_climatiques_robusta, message=FALSE}

# ----------------------------------------------------------

# VARIETY-SPECIFIC CLIMATE INDICES — ROBUSTA GROUP

# Identical pipeline to the Arabica chunk. Only the file

# lists and weight vectors change.

# Robusta group: Vietnam, Indonesia, Uganda, Cote d'Ivoire,

# India, Brazil.

# Mixed producers (Brazil, Indonesia, Uganda, India) contribute

# their Robusta share only via POIDS_ROBUSTA.

# ----------------------------------------------------------

# STEP 1 — READ PRECIPITATION FILES FOR ROBUSTA COUNTRIES

FICHIERS_PRECIP_ROB <- FICHIERS_PRECIP[names(POIDS_ROBUSTA)]

liste_precip_rob <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_PRECIP_ROB,

nom_pays = names(FICHIERS_PRECIP_ROB),

variable = "precip",

SIMPLIFY = FALSE)

df_precip_rob <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_precip_rob) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# STEP 2 — COMPUTE WEIGHTED PRECIPITATION INDEX — ROBUSTA

cols_precip_rob <- paste0("precip_", names(POIDS_ROBUSTA))

df_precip_rob <- df_precip_rob %>%

rowwise() %>%

mutate(indice_precip_robusta = sum(

c_across(all_of(cols_precip_rob)) * POIDS_ROBUSTA,

na.rm = TRUE)) %>%

ungroup()

# STEP 3 — READ TEMPERATURE FILES FOR ROBUSTA COUNTRIES

FICHIERS_TEMP_ROB <- FICHIERS_TEMP[names(POIDS_ROBUSTA)]

liste_temp_rob <- mapply(FUN = lire_climat_pays,

fichier = FICHIERS_TEMP_ROB,

nom_pays = names(FICHIERS_TEMP_ROB),

variable = "temp",

SIMPLIFY = FALSE)

df_temp_rob <- Reduce(function(x, y) left_join(x, y, by = "date"),

liste_temp_rob) %>%

filter(date >= DATE_DEBUT & date <= DATE_FIN) %>%

arrange(date)

# STEP 4 — COMPUTE WEIGHTED TEMPERATURE INDEX — ROBUSTA

cols_temp_rob <- paste0("temp_", names(POIDS_ROBUSTA))

df_temp_rob <- df_temp_rob %>%

rowwise() %>%

mutate(indice_temp_robusta = sum(

c_across(all_of(cols_temp_rob)) * POIDS_ROBUSTA,

na.rm = TRUE)) %>%

ungroup()

# STEP 5 — SAVE TO DISK

df_indice_precip_robusta <- df_precip_rob %>%

select(date, indice_precip_robusta)

df_indice_temp_robusta <- df_temp_rob %>%

select(date, indice_temp_robusta)

write.csv(df_indice_precip_robusta,

file.path(PATH_OUTPUT, "indice_precip_robusta_2000_2023.csv"),

row.names = FALSE)

write.csv(df_indice_temp_robusta,

file.path(PATH_OUTPUT, "indice_temp_robusta_2000_2023.csv"),

row.names = FALSE)

```

The same variety-specific logic applied to the climate indices is now extended to the supply-and-demand fundamentals. Rather than using world totals for production, consumption, exports and ending stocks, two variety-specific aggregates are constructed by summing across the countries assigned to each group, weighted by their variety split. This ensures that the fundamentals used in the Arabica models reflect conditions in Arabica-producing countries only, and vice versa for Robusta.

```{r fondamentaux_arabica, message=FALSE, warning=FALSE}

# ----------------------------------------------------------

# VARIETY-SPECIFIC FUNDAMENTALS — ARABICA GROUP

# Production, consumption, exports and ending stocks are

# aggregated across Arabica-producing countries only.

# Mixed producers (Brazil, India, Uganda, Indonesia) contribute

# their Arabica share only, applied to their country-level

# fundamentals before summing to group totals.

# ----------------------------------------------------------

# Arabica countries with their variety splits

arabica_splits_df <- data.frame(

Country_Name = c("Brazil", "Colombia", "Ethiopia", "India",

"Honduras", "Mexico", "Guatemala", "Peru",

"Nicaragua", "Costa Rica"),

split = c(0.723, 1.000, 1.000, 0.322,

1.000, 1.000, 1.000, 1.000,

1.000, 1.000),

stringsAsFactors = FALSE

)

# Apply variety split to fundamentals and aggregate

df_usda_arabica <- df_usda %>%

filter(Attribute_Description %in% c("Production",

"Domestic Consumption",

"Exports",

"Ending Stocks"),

Market_Year >= 2000, Market_Year <= 2024) %>%

# Recode Cote d'Ivoire before join

mutate(Country_Name = recode(Country_Name,

"Cote d'Ivoire" = "Côte d'Ivoire")) %>%

# Keep only Arabica countries

inner_join(arabica_splits_df, by = "Country_Name") %>%

# Apply variety split to each country's value

mutate(Value_adj = Value * split) %>%

# Sum across countries for each year and attribute

group_by(Market_Year, Attribute_Description) %>%

summarise(valeur = sum(Value_adj, na.rm = TRUE), .groups = "drop") %>%

pivot_wider(names_from = Attribute_Description,

values_from = valeur) %>%

rename(annee = Market_Year,

production_ara = Production,

consommation_ara = `Domestic Consumption`,

exportations_ara = Exports,

ending_stocks_ara = `Ending Stocks`) %>%

arrange(annee) %>%

mutate(consommation_ara = ifelse(annee == 2000, NA, consommation_ara))

# Expand to monthly frequency

df_usda_arabica_monthly <- df_usda_arabica %>%

rowwise() %>%

do({

annee <- .$annee

data.frame(

date = format(seq(as.Date(paste0(annee, "-01-01")),

as.Date(paste0(annee, "-12-01")),

by = "month"), "%Y-%m"),

production_ara = .$production_ara,

consommation_ara = .$consommation_ara,

exportations_ara = .$exportations_ara,

ending_stocks_ara = .$ending_stocks_ara

)

}) %>%

ungroup()

write.csv(df_usda_arabica_monthly,

file.path(PATH_OUTPUT, "fondamentaux_arabica_2000_2023.csv"),

row.names = FALSE)

```

```{r fondamentaux_robusta, message=FALSE, warning=FALSE}

# ----------------------------------------------------------

# VARIETY-SPECIFIC FUNDAMENTALS — ROBUSTA GROUP

# Identical pipeline to the Arabica chunk.

# Robusta countries: Vietnam, Indonesia, Uganda, Cote d'Ivoire,

# India, Brazil — each with their empirical Robusta split.

# ----------------------------------------------------------

# Robusta countries with their variety splits

robusta_splits_df <- data.frame(

Country_Name = c("Brazil", "Vietnam", "Indonesia", "India",

"Uganda", "Cote d'Ivoire"),

split = c(0.277, 1.000, 0.877, 0.678,

0.809, 1.000),

stringsAsFactors = FALSE

)

# Apply variety split to fundamentals and aggregate

df_usda_robusta <- df_usda %>%

filter(Attribute_Description %in% c("Production",

"Domestic Consumption",

"Exports",

"Ending Stocks"),

Market_Year >= 2000, Market_Year <= 2024) %>%

# Keep original Cote d'Ivoire spelling for join

inner_join(robusta_splits_df, by = "Country_Name") %>%

# Apply variety split to each country's value

mutate(Value_adj = Value * split) %>%

# Sum across countries for each year and attribute

group_by(Market_Year, Attribute_Description) %>%

summarise(valeur = sum(Value_adj, na.rm = TRUE), .groups = "drop") %>%

pivot_wider(names_from = Attribute_Description,

values_from = valeur) %>%

rename(annee = Market_Year,

production_rob = Production,

consommation_rob = `Domestic Consumption`,

exportations_rob = Exports,

ending_stocks_rob = `Ending Stocks`) %>%

arrange(annee) %>%

mutate(consommation_rob = ifelse(annee == 2000, NA, consommation_rob))

# Expand to monthly frequency

df_usda_robusta_monthly <- df_usda_robusta %>%

rowwise() %>%

do({

annee <- .$annee

data.frame(

date = format(seq(as.Date(paste0(annee, "-01-01")),

as.Date(paste0(annee, "-12-01")),

by = "month"), "%Y-%m"),

production_rob = .$production_rob,

consommation_rob = .$consommation_rob,

exportations_rob = .$exportations_rob,

ending_stocks_rob = .$ending_stocks_rob

)

}) %>%

ungroup()

write.csv(df_usda_robusta_monthly,

file.path(PATH_OUTPUT, "fondamentaux_robusta_2000_2023.csv"),

row.names = FALSE)

```

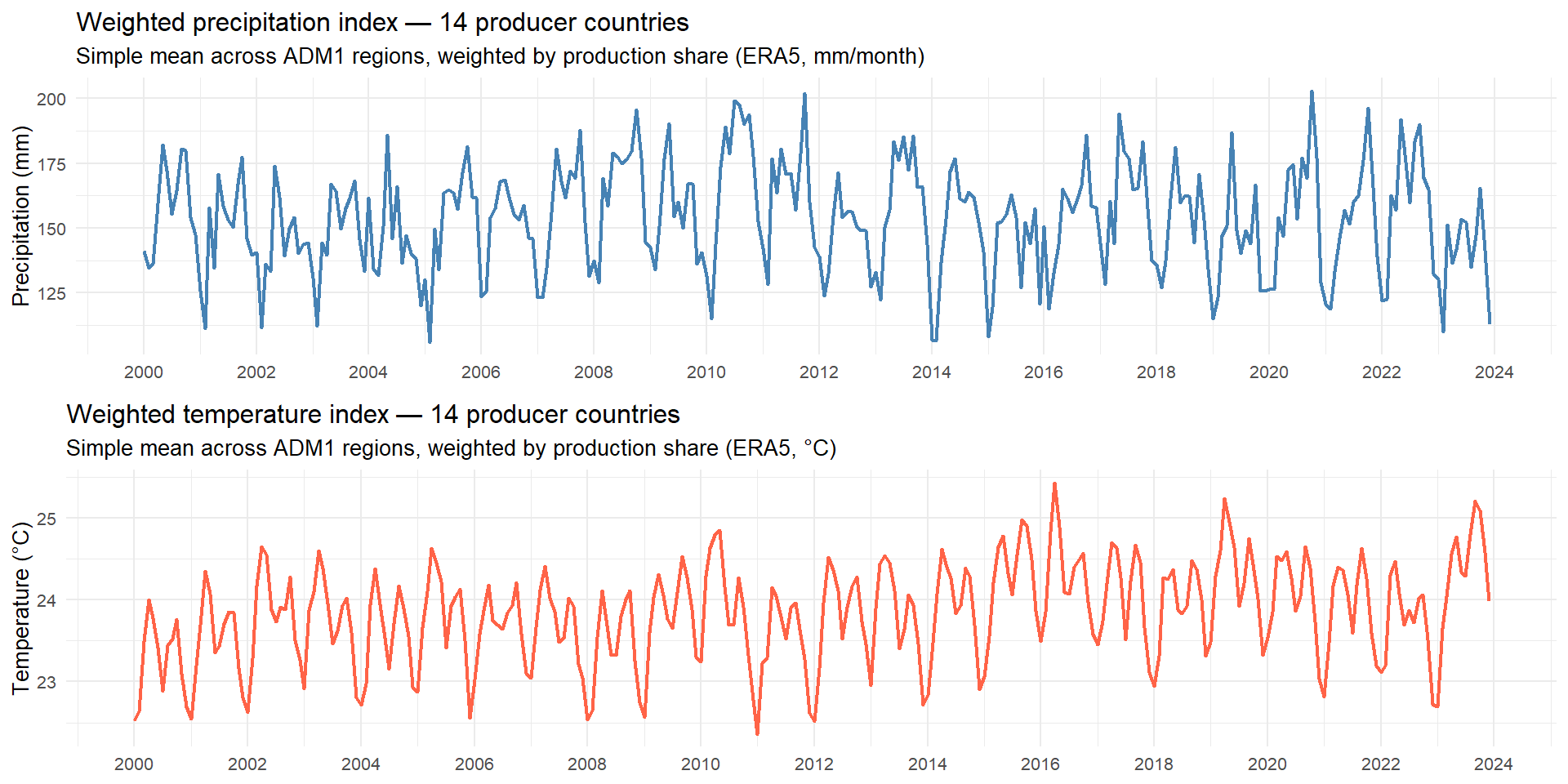

This chunk joins the two climate indices into a single plotting frame and produces a two-panel time series chart for visual inspection. The plot serves as a first diagnostic check on the indices: it allows verifying that the seasonal patterns, trend behaviour and known climate episodes visible in the raw data are correctly reflected in the aggregated series before they enter the modelling pipeline.

```{r plot_climat, fig.width=10, fig.height=5}

# ----------------------------------------------------------

# BUILD THE PLOTTING FRAME

# The two index series are joined on date and a proper Date

# column is added for ggplot's date scale. Both indices are

# already filtered to 2000-2023 from the previous chunks,

# so no further filtering is needed here.

# ----------------------------------------------------------

df_clim_plot <- df_indice_precip %>%

left_join(df_indice_temp, by = "date") %>%

mutate(date_fmt = as.Date(paste0(date, "-01")))

# ----------------------------------------------------------

# TWO-PANEL CLIMATE INDEX PLOT

# Panel 1 — Precipitation index (mm/month)

# A strong seasonal cycle is expected and confirms that the

# ADM1 averaging and weighting steps preserved the seasonal

# signal present in the raw country-level data.

#

# Panel 2 — Temperature index (°C)

# A gradual upward trend over the period is consistent with

# documented warming in tropical producing regions. If

# confirmed by the stationarity tests below, this trend

# implies that the temperature series will require first-

# differencing before entering the econometric models.

# ----------------------------------------------------------

gridExtra::grid.arrange(

ggplot(df_clim_plot, aes(date_fmt, indice_precip)) +

geom_line(color = "steelblue", linewidth = 0.8) +

labs(title = "Weighted precipitation index — 14 producer countries",

subtitle = "Simple mean across ADM1 regions, weighted by production share (ERA5, mm/month)",

x = NULL, y = "Precipitation (mm)") +

theme_minimal(base_size = 10) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y"),

ggplot(df_clim_plot, aes(date_fmt, indice_temp)) +

geom_line(color = "tomato", linewidth = 0.8) +

labs(title = "Weighted temperature index — 14 producer countries",

subtitle = "Simple mean across ADM1 regions, weighted by production share (ERA5, °C)",

x = NULL, y = "Temperature (°C)") +

theme_minimal(base_size = 10) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y"),

ncol = 1

)

```